TAX IMPLICATIONS FOR MARRIAGES IN COMMUNITY OF PROPERTY

The default marriage regime has some complicated tax consequences.

When couples are caught up in wedding and honeymoon planning, visiting their attorney often takes a backseat.

Many couples don’t realise that different marital laws affect how their assets are managed during marriage, divided if it ends, and how they’re taxed.

SARS made some updates to the 2023 personal income tax return. While most reporting requirements stay the same, the way SARS verifies the information is what’s drawing the most attention.

If you are married in community of property, a separate section for spouse details is opened, in which SARS requires your spouse’s initials and their ID number.

However, providing these details is more than a simple box-ticking exercise.

These include investment income (interest and dividends, both local and foreign), rental income, and capital gains and losses.

If you’re married in community of property, you’re taxed on half of your own and half of your spouse’s interest, dividends, rental income, and capital gains.

For any investment income that has not pulled through from a third-party upload, as well as for any rental income and capital gains or losses, you will need to provide the full amount of income received by both spouses in both of your tax returns.

SARS will automatically divide this income on a 50/50 basis.

This will be reflected on the notices of assessment (ITA34) issued to both you and your spouse once the returns have been submitted. Your returns do not need to be submitted simultaneously to achieve this split.

Some income types, by law, aren’t included in the community of property.

For instance, if someone inherits property or investments, and the deceased’s will specifically states it’s outside the communal estate, then it’s excluded.

Salaries have been taxed separately since the tax tables were harmonised in the early 1990s. This applies irrespective of one’s marital status.

If you and your spouse are separated and such separation is likely to be permanent, you would need to submit an RRA01 form to SARS or lodge an objection against your return.

If you and your spouse are divorced and you had omitted to amend your marital status from married in community of property to not married.

SARS will issue an amended assessment but is likely to request an upload of your divorce decree—particularly if the divorce was recent and the Home Affairs records have not yet been updated.

New SARS Forex Regulations for Foreign Income Earners

South Africans who earn their income in a foreign currency and their employers will soon face a lot more red tape with the South African Revenue Service (SARS), which could discourage international companies from hiring South Africans.

The National Treasury has proposed new foreign exchange regulations for South Africans who work for a foreign company and earn their income in a foreign currency.

Previously, when a South African was earning money abroad, it was their responsibility to pay provisional tax in South Africa.

For example, a taxpayer who earned dollars in an offshore account because they did services for an American company had to declare this money to SARS, convert it to rands and pay their taxable income from these rands.

However, the National Treasury thought this system could simply be sidestepped by taxpayers not declaring their forex earnings.

Therefore, foreign companies employing South Africans now have to form a sub-branch in South Africa, register via the Companies and Intellectual Property Commission, and register for pay-as-you-earn tax on their employee’s behalf.

The red tape that comes with these new regulations could see foreign companies go one of two ways.

Firstly, they could say, “South Africans were great and cheap, but unfortunately, the red tape has made this too onerous for us, and we have to cut ties with South African employees.”

Alternatively, foreign companies enter the market and register in South Africa as the South African leg for foreign entities, becoming essentially ‘intermediaries’ that will handle SARS and the National Treasury on behalf of foreign companies.

South African employees of these companies could also find ways to simplify the new regulations.

For example, the employees could register a company in South Africa and outsource themself as a company to foreign entities, which would sidestep the proposed regulations.

These regulations have not been passed yet and are still open for comment – 2023AnnexCProp@treasury.gov.za/ acollins@sars.gov.za

Receiving Rental Income? [A MUST READ]

What is rental income?

If an individual rents out a property (generally residential accommodation) and receives rental income, the amount received will be subject to income tax.

Residential accommodation can include:

- holiday homes

- bed-and-breakfast establishments

- guesthouses

- renting a section of your home, e.g. a room or a garden flat.

- dwelling houses and

- other similar residential dwellings.

How is tax calculated on rental income?

The rental income you receive should be added to any other income you may have but will also be reduced by certain permissible expenses incurred.

If any other amounts are paid to you for the rental of residential accommodation, in addition to the monthly rental, these amounts will also be subject to income tax.

The additional amounts can include, for example, lease premiums which are usually paid in the form of a lump sum at the start of the lease, in which case the full amount is subject to tax in the year of assessment during which it accrues or is received, whichever is the earlier.

The receipt or accrual of a rental deposit by a lessor need not be included in the lessor’s gross income at the stage it is initially paid, if there is an obligation on the lessor to refund the deposit at a later stage.

It will generally only become gross income in the lessor’s hands when the deposit is eventually applied by the lessor.

The treatment of a rental deposit should, however, be determined on the specific facts and circumstances of each case.

If you are married in community of property, please ensure both spouses are submitting their annual returns declaring their rental income and expenses.

If the property is owned jointly, please state your ownership percentage. Therefore, the profit/loss is apportioned accordingly.

Can the rental income be reduced?

Yes, the rental income may be reduced by any permissible expenses incurred during the period that the property was let.

Only expenses incurred in the production of that rental income can be claimed.

Any capital and/or private expenses will not be allowed as a deduction.

Which expenses are permissible?

Permissible expenses that may be deducted from rental income could include:

- rates and taxes

- levies

- water and electricity

- subscriptions

- accounting fees

- building insurance for property let out

- bond interest

- advertisements

- agency fees of estate agents

- insurance (only homeowner’s insurance and not insurance for household contents or bond insurance)

- garden services and cleaning

- repairs in respect of the area let and

- security and property levies

Which expenses are not allowed?

Expenses that are capital in nature or that are not in the production of rental income will not be allowed.

These can include, for example, costs for improvements made to the property.

Improvements should not be confused with repairs and maintenance which are allowed as a deduction.

Repairs and maintenance would usually take place when a person attempts to restore an asset to its original condition as a result of damage or deterioration.

Improvements would usually result in the creation of a better asset.

To determine whether a repair, maintenance or improvement has taken place, the specific facts and circumstances of each case must be examined.

While improvements are not allowed as a deduction against rental income, the value thereof can, however, be included in the base cost of the property, to effectively reduce the capital gain (or loss) on the eventual disposal of the property, for capital gains tax purposes.

The supply of accommodation in a dwelling is an exempt supply for VAT purposes, and consequently you may not deduct any VAT incurred on expenses in respect of supplying accommodation in a dwelling.

What if the expenses exceed the rental income?

Should the expenses exceed the rental income, the loss should be available for set-off against other income earned by the individual, provided that the loss is not “ring-fenced” in terms of prevailing anti-avoidance provisions.

The individual must effectively be able to satisfy SARS that he or she is carrying on a bona fide trade through the rental of his or her property.

If it is a shared property, please ensure that you state the square meterage of the entire property as a whole and the portion of the property been leased out.

Please note that you can only claim the portion of the expense of the leased property. Personal property expenses are not tax deductible.

Important Notice: Lease Agreements

Upon audit, SARS is calling for your fully signed and witnessed lease agreements.

Please ensure you have an updated lease agreement in place.

SARS is also inspecting the lease agreement to see which expenses the responsibility of the lessee and which expenses are the responsibility of the lessor.

Therefore, please ensure that the expenses you are paying for (the Landlord) is clearly stipulated in your agreement that you are responsible and paying for (ie: rates, security, levies, utilities, repairs, garden services)

If SARS is not satisfied that an expense is incurred for the leased property, they will disallow it.

SARS is also checking to see if your rental property is market related and if you are making reoccurring losses each year, you will have to provide reasons for this.

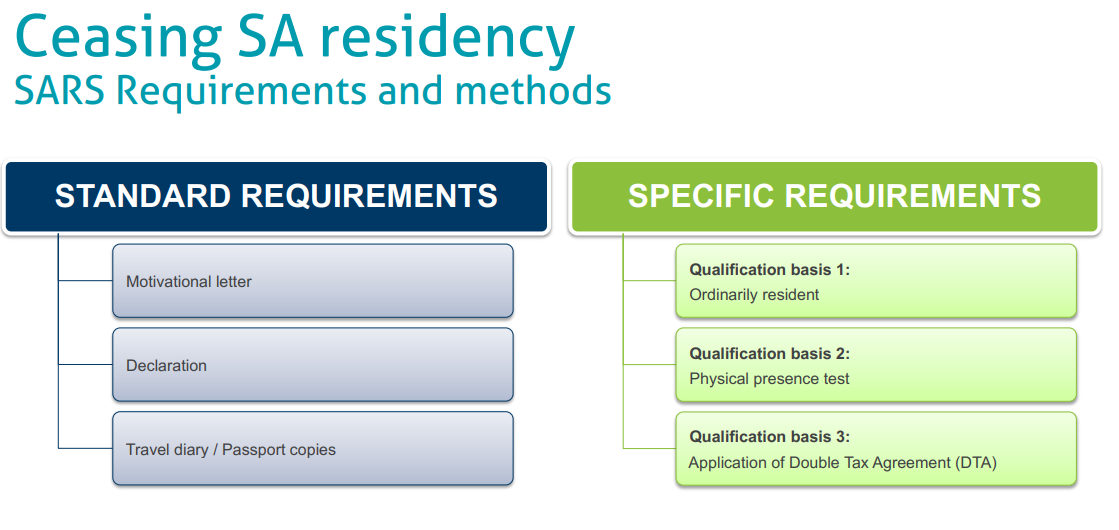

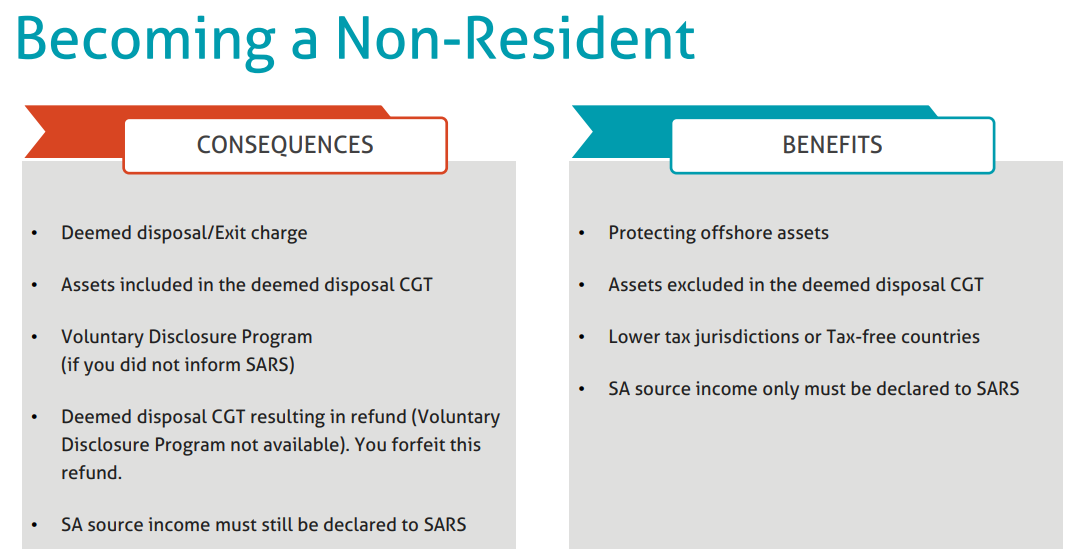

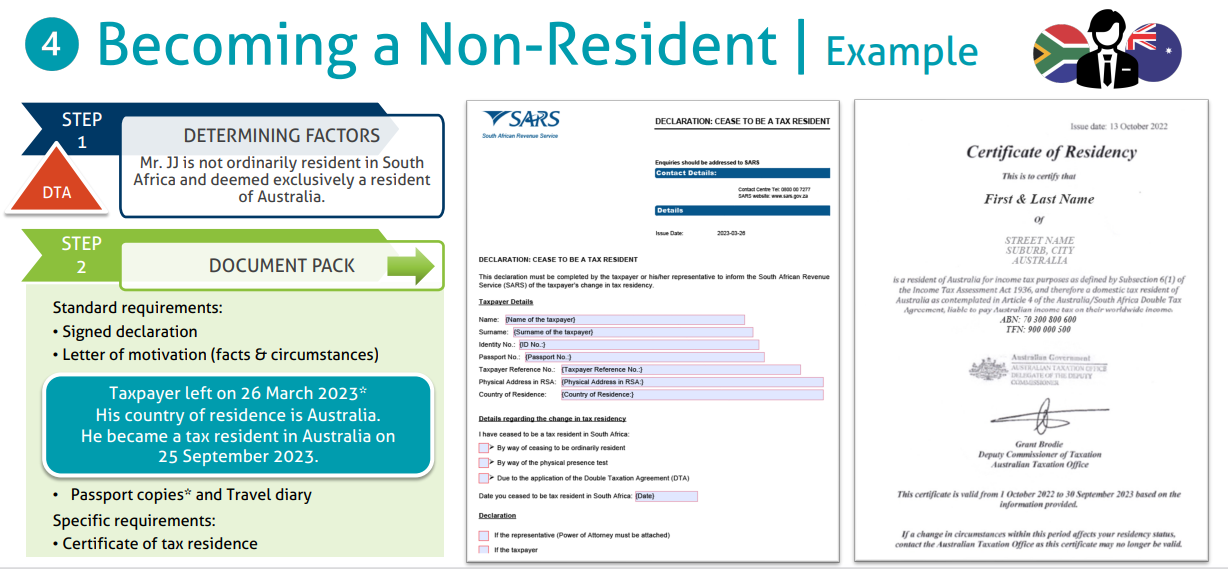

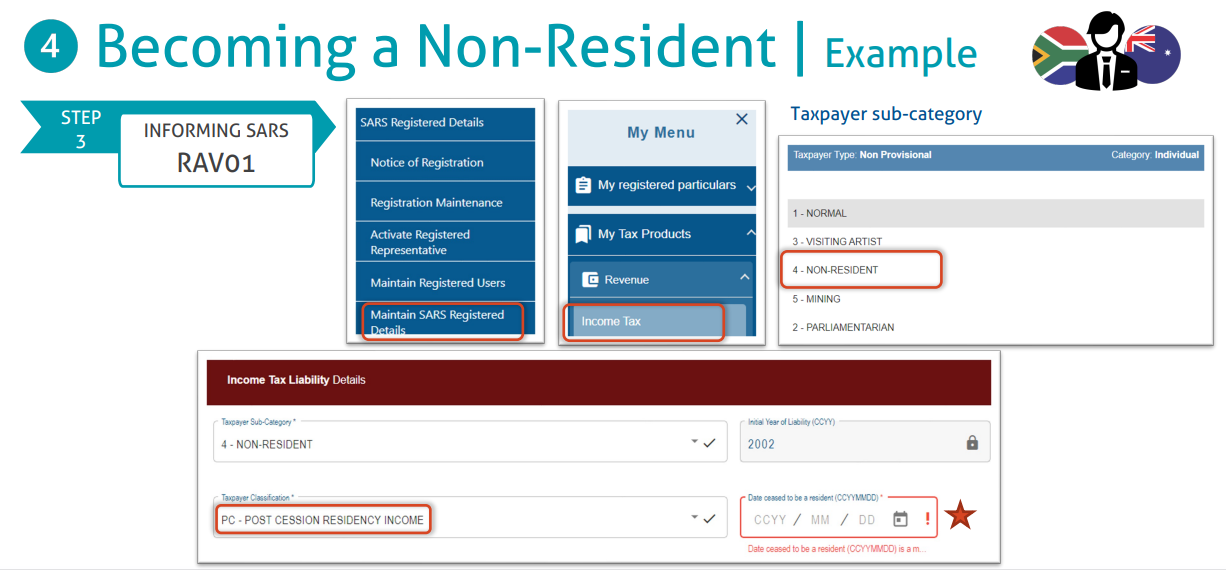

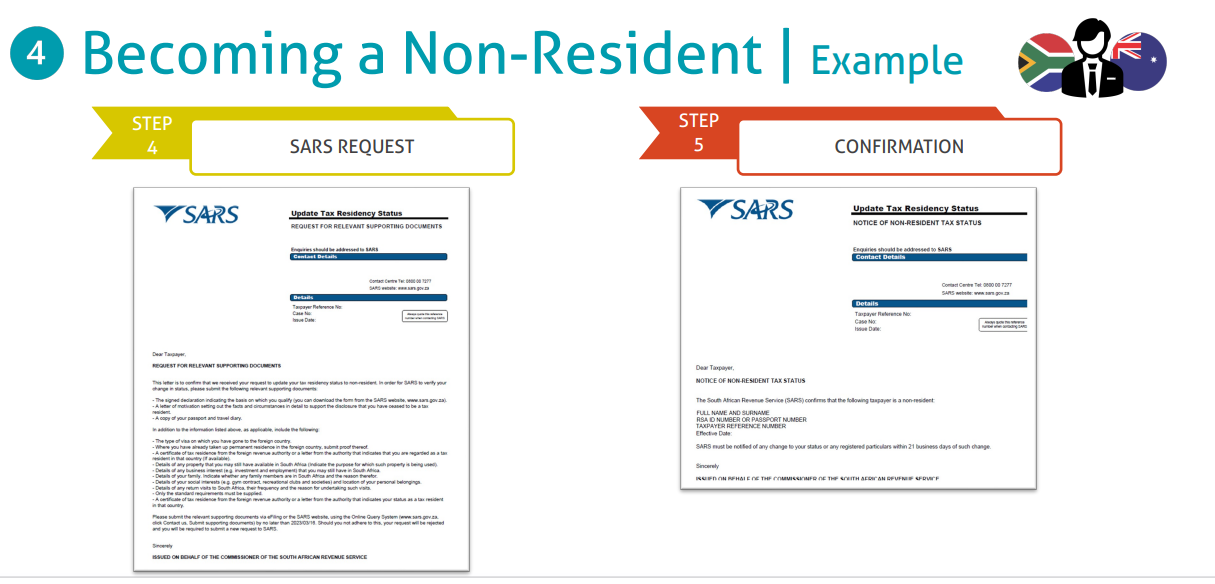

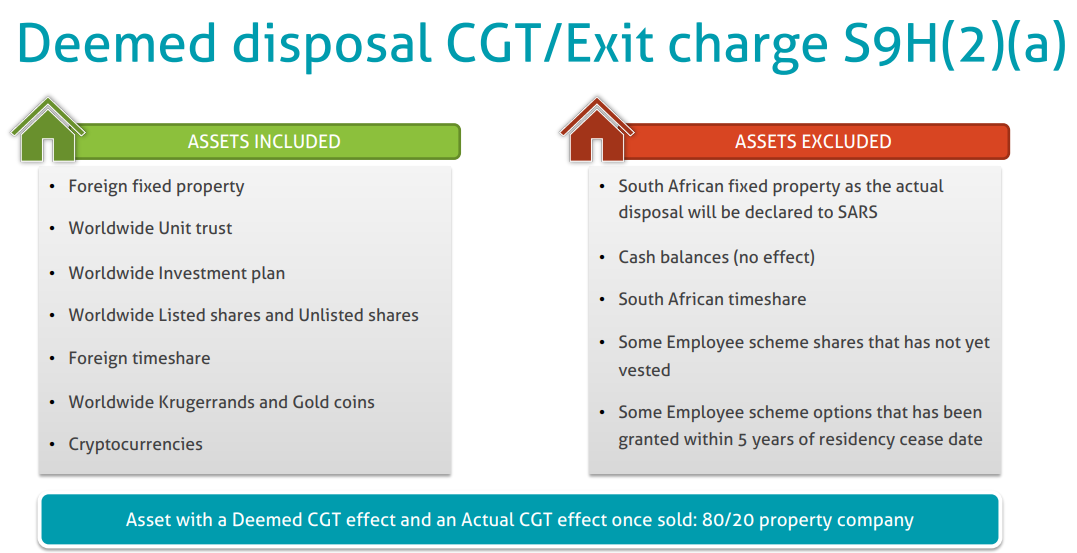

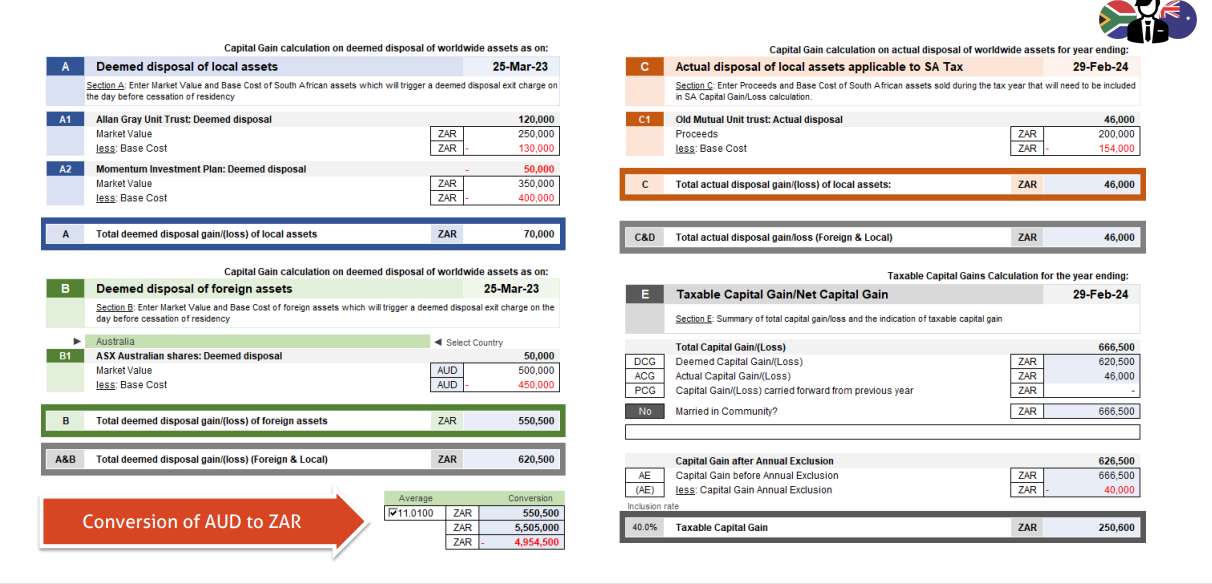

Everything you need to know about Ceasing your South African Residency.

This post includes:

- SARS Requirements and methods

- How to become a Non-Resident (Consequences and Benefits)

- Supporting Documents

- How to inform SARS

- Disposal CGT and Exit Charge explained, with examples.

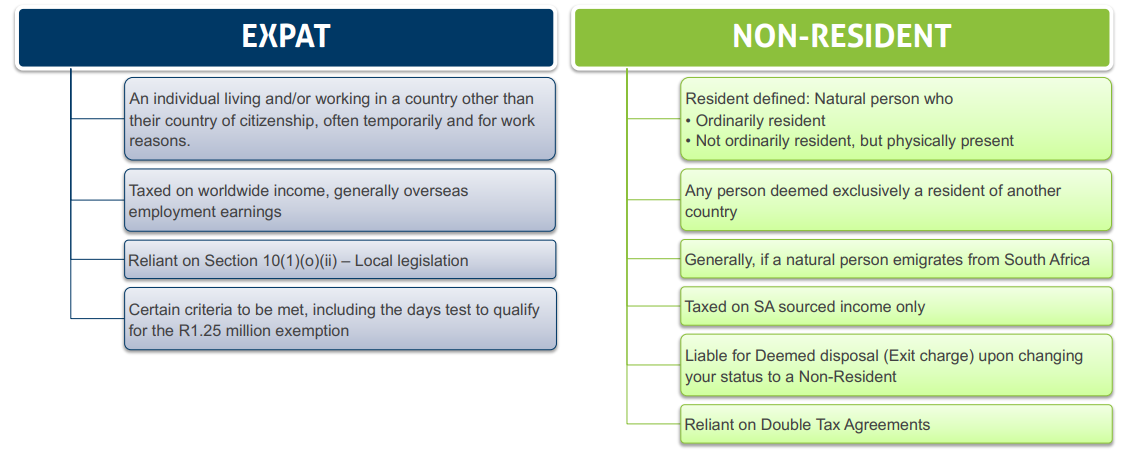

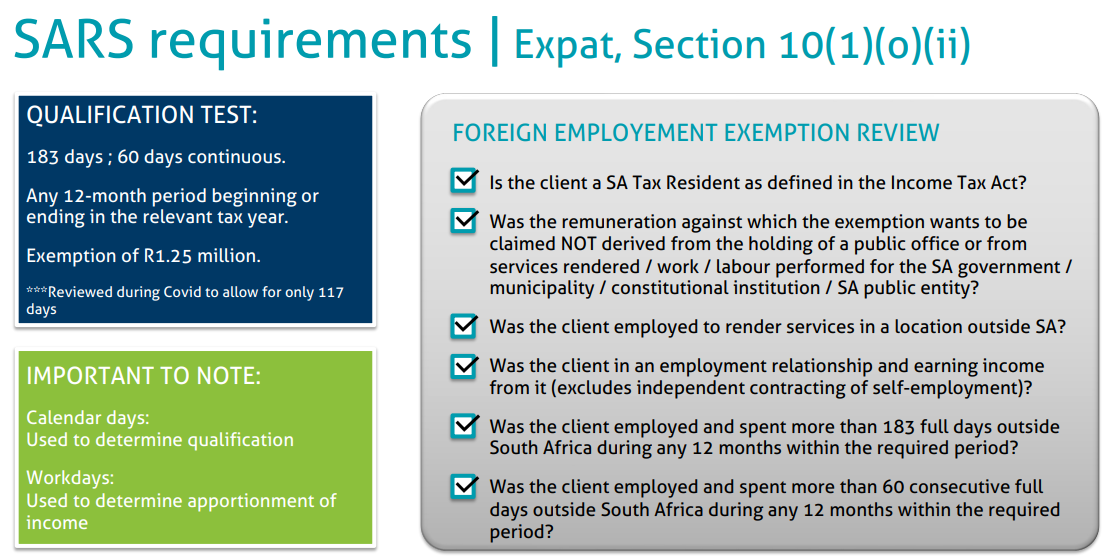

Everything you need to know about Expatriate Taxes and SARS Requirements:

- Includes: Expat Checklist Criteria

- Qualification Test

- Foreign Employment Exemption Review

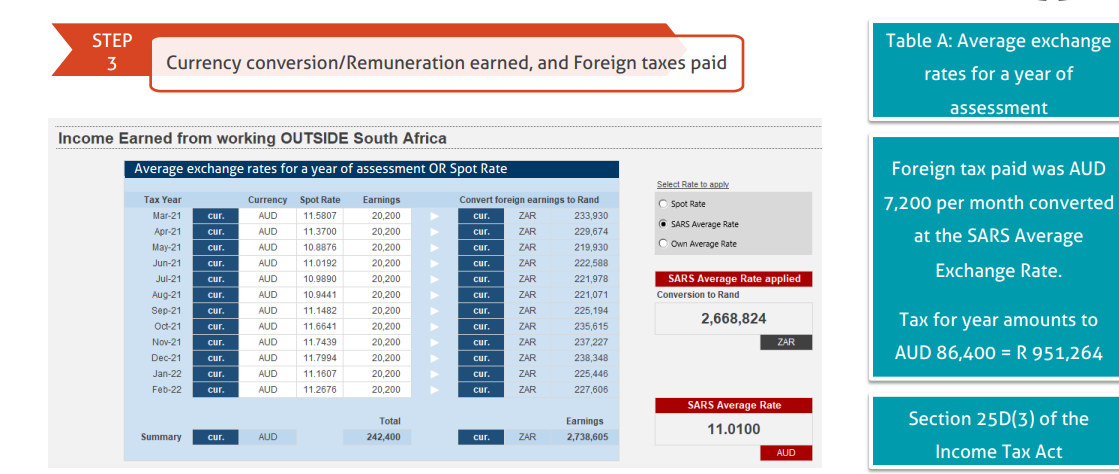

- Currency Conversion Guide

- How to calculate Your Foreign Taxable Income

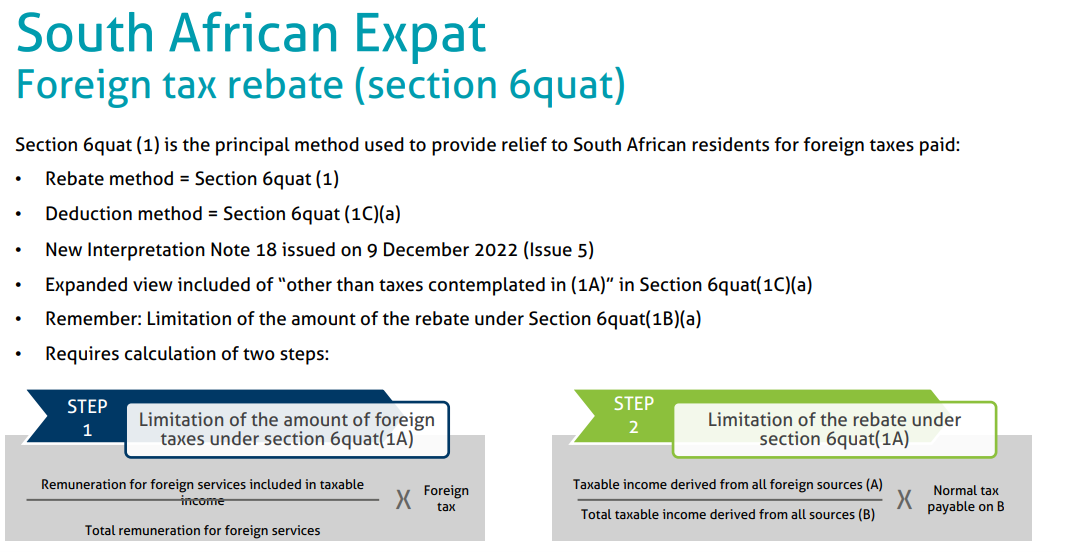

- How to calculate Your Foreign Tax Rebate

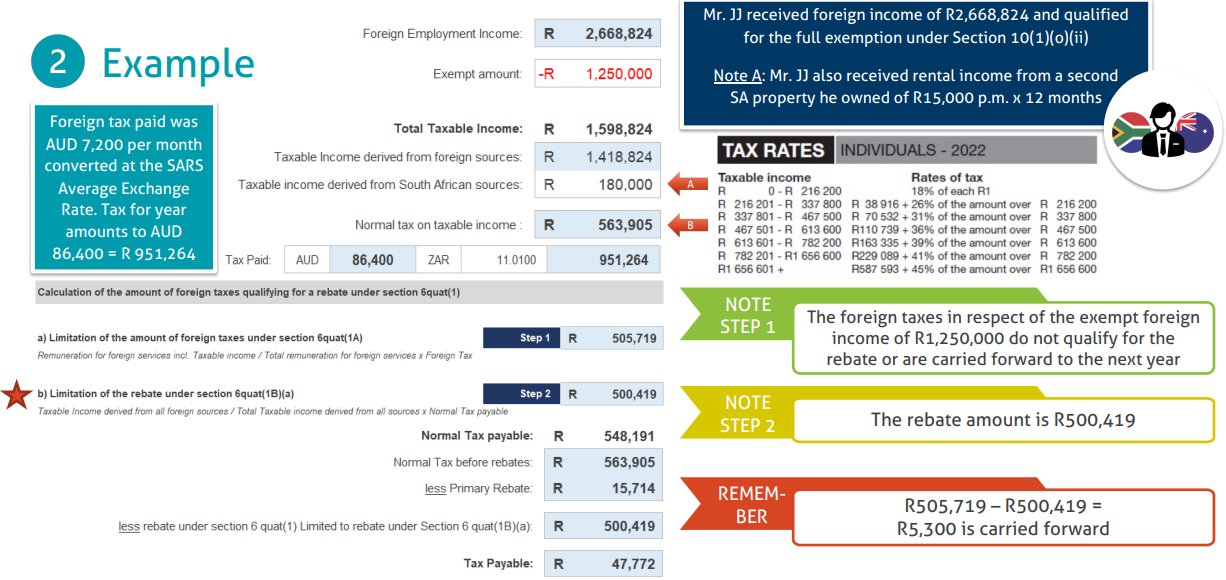

- Additional notes and SARS Tax Rates

2023-06-09 WWTS EXPAT TAX GUIDE

2023-05-26 Worldwide Tax Solutions Newsletter – Forex Trading and Donations Tax

WWTS BUDGET GUIDE – 2023/2024