SARS to Access more Bank Accounts to curb Non-Compliance in 2026

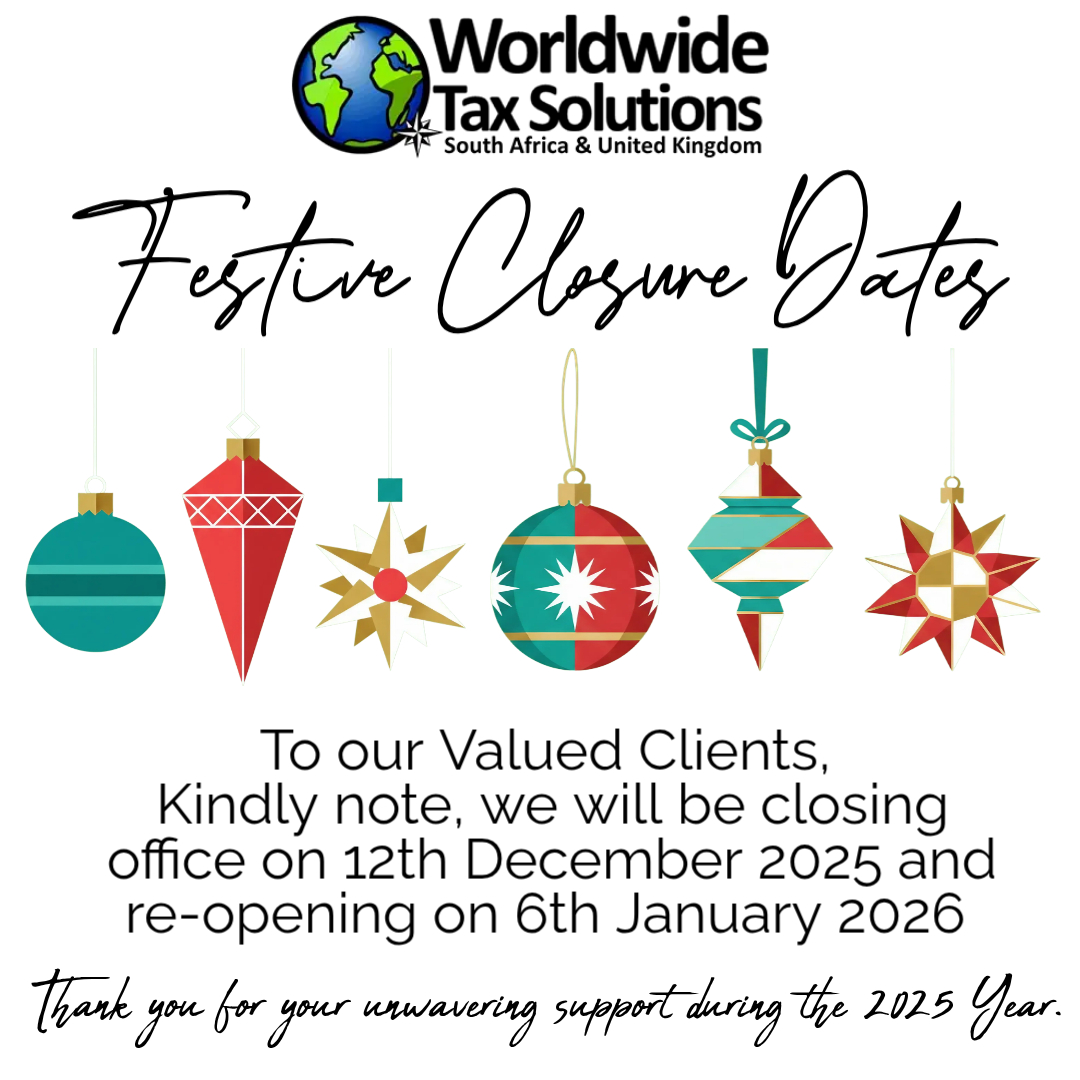

Our Christmas Closure Dates

Worldwide Tax Solutions Newsletter – Smart Holiday Savings & Tax-Savvy Tips for South Africans

As the festive season approaches, it’s common for spending to rise travel, family gatherings, gifts, and year-end events all add up.

With a few mindful habits and some strategic tax planning, you can enjoy the holidays while keeping your financial health on track.

Here’s your practical guide to spending wisely and preparing for a more tax-efficient year-end.

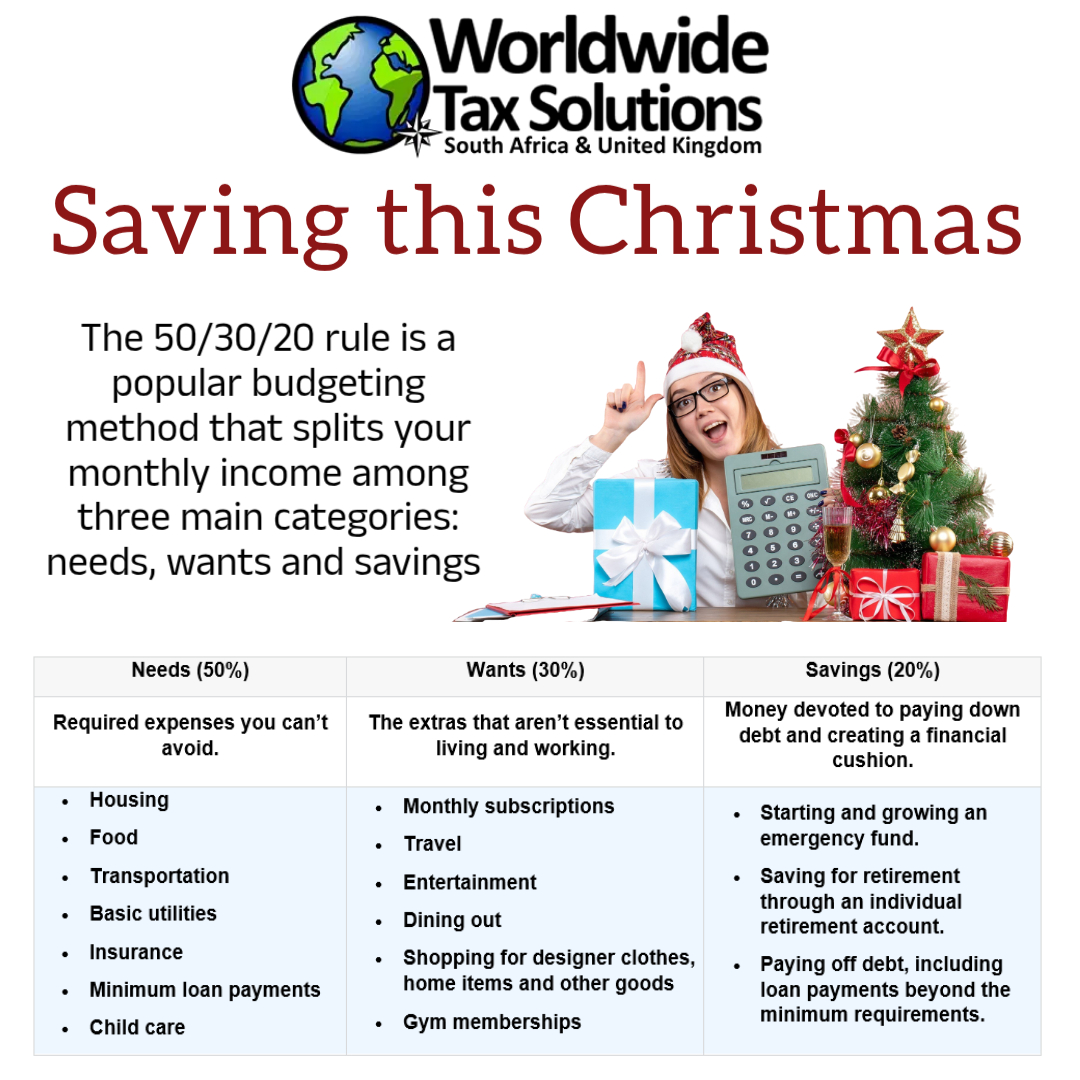

Set a Festive Budget That Actually Works

South Africans often underestimate holiday costs, especially with seasonal price increases.

Tips to stay in control:

- Create a budget for gifts, food, travel, and entertainment.

- Use loyalty programmes (eBucks, Vitality, Smart Shopper, UCount) to reduce costs.

- Shop earlier to avoid “last-minute inflation” from surge pricing and limited stock.

Consider Cost-Effective, Meaningful Gifting

Thoughtful doesn’t mean expensive.

Ideas:

- Give personalised or handmade items.

- Suggest family gift draws instead of buying for everyone.

- Compare prices using local apps and online stores to avoid overspending.

Make Use of Tax-Efficient Investment Products Before 28 February

South Africa’s tax year ends on 28 February meaning the festive season is a perfect time to review contributions.

Consider topping up:

- Retirement Annuities (RAs): Contributions may be tax-deductible topping up before tax year-end can lower your taxable income.

- Tax-Free Savings Accounts (TFSAs): While contributions aren’t deductible, growth and withdrawals are tax-free.

- Endowments: Useful if you’re in a higher tax bracket and want tax-efficient long-term investing.

If you’d like, I can include this year’s exact contribution limits.

Be Strategic With Charitable Giving

Giving is a big part of the holiday spirit and SARS may offer tax benefits.

Consider:

- Donations to S18A-approved organisations may qualify for tax deductions.

- Always request an S18A certificate for your records.

- Year-end is a good time to “bunch” charitable donations to maximise the deduction.

Review Your Medical Scheme & Medical Expenses

Medical expenses often spike during December due to year-end travel and festive activities.

Tax considerations:

- Keep receipts for qualifying out-of-pocket medical expenses.

- Make sure you understand your medical scheme’s year-end benefits, gap cover rules, and thresholds.

- If you’re approaching the end of the tax year, additional qualifying expenses may help you claim a portion back.

Check Your Tax Withholding Before February

If you received a large refund last year or an unexpected bill adjusting your PAYE or provisional tax now can help you avoid surprises.

A quick review can ensure your tax profile is accurate before SARS’s February deadline.

Plan for Holiday Travel Wisely

Travel is one of the biggest December costs.

Ways to save:

- Book in advance or travel slightly off-peak when possible.

- Compare domestic routes and carriers prices can vary widely.

- Look for fuel rewards if driving long distances.

Get a Head Start on Your 2025 Financial Plan

The new year is a perfect opportunity to refresh your financial strategy.

Consider reviewing:

- Your emergency fund

- Your investment and savings goals

- Your tax position ahead of February year-end

- Short-term debt and credit use over the holidays

Small adjustments now can create a more secure financial year ahead.

We’re Here to Help

If you’d like personalised year-end tax planning or help reviewing your investment strategy before the 28 February deadline, we’re here to guide you.

Wishing you a joyful, financially confident holiday season!

– Your Advisory Team @Worldwide Tax Solutions

How SARS can Appoint a 3rd Party to recover your Tax Debt

The South African Revenue Service (SARS) uses a mechanism called a Third Party Notice (AA88), which functions similarly to a garnishee order, to collect outstanding tax debt directly from a taxpayer’s employer or bank.

How SARS Third Party Notices Work

- Legal Basis: This action is taken under the Tax Administration Act 28 of 2011.

- Direct Collection: The notice instructs a third party (e.g., an employer, bank, or pension fund) who holds money on behalf of the taxpayer to pay that money directly to SARS in satisfaction of the tax debt.

- Employer’s Obligation: An employer receiving a valid Third Party Notice is legally obligated to comply and deduct the specified amount from the employee’s salary.

- Without Prior Court Order (sometimes): While a general garnishee order (or emoluments attachment order) from a normal creditor typically requires a court order signed by a magistrate, SARS has specific powers under the Tax Administration Act to issue a Third Party Notice directly to an agent (like a bank or employer) to collect outstanding tax debt.

- Notification: The taxpayer should be notified of the outstanding debt and the intended action, giving them a chance to make a payment plan. The third party (employer/bank) also receives the notice.

How to Dispute or Manage a SARS Notice

If you receive a Third Party Notice from SARS, you have rights and options to address it:

- Verify the Debt: Ensure the amount claimed is correct and you genuinely owe the tax debt.

- Contact SARS Immediately: The best way to manage this is to communicate with SARS and, if possible, establish a formal, affordable payment plan.

- Request Affordability Review: If the deduction amount leaves you without enough money to cover basic living expenses, you or your employer can notify SARS and request an affordability assessment. SARS can then cancel the original notice and issue a new one with revised, affordable terms.

- Challenge the Validity: You can challenge the notice if there are procedural errors, the debt is incorrect, or you were not properly notified. This may involve visiting a SARS branch or seeking legal advice.

- Legal Assistance: Consulting with a tax practitioner or legal professional can help you navigate the process, verify the order’s validity, and, if necessary, apply to the court to have it varied or set aside.

Prevention is key: Ensure your tax returns are filed on time and any liabilities are paid to avoid penalties and enforcement actions like Third Party Notices.

Can a payment arrangement be made with SARS?

You may request and enter into an instalment payment arrangement with SARS. It allows you to pay your outstanding debt in one sum or in instalments over time until you have paid your entire debt including applicable interest. This agreement however would be subject to certain qualifying criteria.

NEW: SARS Commits to Expedited Tax-Debt Compromise Process – Eff. 18 Oct 2025

SARS holding Wealthy Taxpayers Accountable – Especially if they want to leave the Country

Tax Residency – Everything you need to know

SARS Scores R15 Billion Pay Day, as SA Workers Dip into Two-Pot Retirement funds.

2025-09-22 Worldwide Tax Solutions Newsletter – Tax Savvy in SA

📌 SARS Crackdown on Offshore Assets

SARS continues to exchange financial data with over 100 countries. If you hold offshore investments, ensure they are fully disclosed to avoid hefty fines.

💰 Tax-Smart Tips

- Use Your Medical Tax Credits

Keep receipts for medical aid, out-of-pocket expenses, and chronic medication – these can reduce your tax bill. - Maximise Retirement Contributions

Contributions to pension, provident, or retirement annuity funds are deductible up to 27.5% of taxable income (capped at R350,000 per year). - Home Office Deductions

If you work from home, part of your rent, internet, electricity, and cleaning costs may be deductible – provided you meet SARS’s strict criteria. - Provisional Tax Planning

If you earn income outside of a salary (like rental, freelance, or business income), make sure your provisional tax estimates are realistic to avoid underpayment penalties.

🌍 For South Africans Abroad

- If you spend more than 183 days outside SA (60 consecutive) and meet the physical presence test, you may qualify for the foreign employment income exemption under Section 10(i)(o)(ii).

- However, SA residents are taxed on worldwide income unless formally ceased residency. Get professional advice before assuming you’re exempt from Worldwide Tax Solutions

📊 Did You Know?

- Small business owners can qualify for Turnover Tax, a simplified tax system if your annual turnover is under R1 million.

- Donations up to R100,000 per year per individual are exempt from Donations Tax.

📌 Action Step for This Month

Check your IRP5 and third-party data on SARS eFiling – SARS already has much of your information. Ensure it matches your own records to prevent disputes.