The tax season dates are not yet announced. However, based on prior years, they are expected to be the following:

01 July 2024 to 23 October 2024: individual (non-provisional) taxpayers

01 July 2024 to 24 January 2025: provisional taxpayers

Here are the top 5 reasons why you should not skip filing your tax return this season:

- You miss out on your refund.

A refund is money you overpaid on your taxes and it belongs to you. You can only get a refund if you file a return. Something as simple as claiming Medical expenses or working for less than 12 months of the tax year can trigger a tax refund, depending on your situation.

- You may not be able to borrow money.

If you wish to borrow money in the form of a mortgage for a home, or a long-term loan of any kind in future, you may need a Tax Compliance Certificate. This can only be obtained if all your returns are up to date and filed appropriately.

- SARS might change their mind.

If you normally submit, but this year you don’t, SARS could administer administrative penalties later on down the line for not being compliant, and no one wants that!

- You can’t access your retirement fund.

Filing a tax return each and every year means that should you receive a payout from a fund at any stage, then you will not have any hassle in getting the money. If you retire or are retrenched, or just need to take money out of your fund early, you need to be tax compliant.

- A complete tax record stands in your favor.

Having an unbroken filing record leaves SARS officials with no reason to suspect that you are hiding information from them. Filing a tax return means you are being a good citizen and contributing towards society.

Medical Expenses

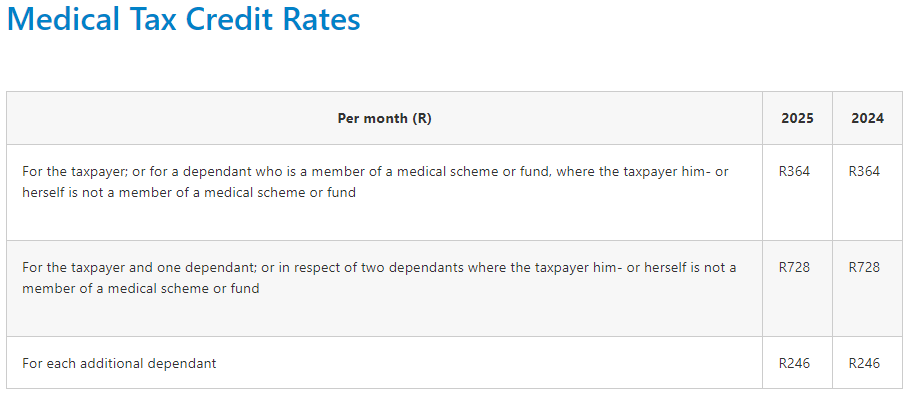

If you contribute to a Medical Aid, you will receive a fixed monthly tax credit for each member on your policy. SARS calls this rebate the Medical Schemes Fees Tax Credit – it is a flat rate per month (i.e. it doesn’t take your taxable income into consideration) and is a direct deduction off your tax liability. Note that the tax credit applies only to registered medical aid funds – medical insurance or GAP cover does not count.

Make sure that you have a tax certificate from your medical aid provider as support for this tax credit. They generally send these out on email before filing season opens.

If you have ‘qualifying’ medical expenses, which were not reimbursed by the medical aid, you should also include these in your tax return because you may qualify for an ‘additional medical expenses tax credit’. Qualifying medical expenses includes all consultations with medical practitioners as well as doctor prescribed medication. SARS applies a complicated formula to work out whether you spent enough to qualify for an ‘additional medical expenses tax credit’.

Remember to ensure you have proof for every single medical expense you paid for over and above your medical aid cover with invoices and / or detailed receipts.

Your medical scheme provider is supposed to send your tax certificate to you by email or post by July, but if they have not done so, you can ask for it directly.

A tax credit is a non-refundable rebate. This means that a portion of your qualifying expenses, in this case medical related spend, is converted to a tax credit, which is deducted from your overall tax liability (the amount of tax you have to pay SARS). You can’t carry any unused credit over to the next tax year and it won’t ever result in a negative amount or standalone refund from SARS.

This means that if you don’t earn an income, but do contribute a medical aid, you can’t claim the medical credit.

Who SARS Considers as Dependents for Medical Expense Claims

SARS sees the following as dependents:

- A spouse (husband or wife)

- A child and the child of a spouse (e.g. son, daughter, stepchild or children, adopted child or children) who was alive during any part of the year of assessment, and provided that on the last day of the year of assessment he / she was unmarried and:

- a minor, i.e. under the age of 18, or

- under 21 years of age, but partly or entirely dependent on you for maintenance and not yet liable for normal tax themselves, or

- under 26 years of age, but partly or entirely dependent on you for maintenance, not yet liable to pay normal tax themselves and a full-time student at a publicly recognized educational institution such as a university or Technikon

- Any other member of your family who relies on you for family care and support (e.g. mother, father, sibling, mother or father-in-law, grandparent or grandchildren)

- Any other person recognized as a dependent in terms of the rules of a medical scheme or fund

- Proof of above payments will be required to claim the medical expenses if the dependent is not directly on your medical aid, however you do pay for their medical expenses

What are Qualifying Medical Expenses for Tax?

Examples of qualifying medical expenses are any amounts that were paid by you, as the taxpayer, during the year of assessment:

- For professional services rendered and medicines supplied by a registered medical practitioner, dentist, optometrist, homeopath, naturopath, osteopath, herbalist, physiotherapist, chiropractor or orthopedist to you or any of your dependent(s)

- To a nursing home or hospital, or any duly registered or enrolled nurse, midwife or nursing assistant (or to any nursing agency in respect of the services of such a nurse, midwife or nursing assistant) in respect of the illness or confinement of the person or any dependent of the person

- For medicines prescribed by a registered medical practitioner and acquired from a pharmacist

- Medical expenses incurred and paid outside South Africa

- It’s important to note that “over the counter” medicines – such as cough syrups, headache tablets or vitamins don’t qualify as medical expenses – unless specifically prescribed by a registered medical practitioner and acquired from a pharmacist.

SARS is strict on the definition of a qualifying disability. According to the Income Tax Act, a disability is:

A moderate to severe limitation of that person’s ability to function or perform daily activities, as a result of a physical, sensory, communication, intellectual or mental impairment if the limitation:

- Has lasted or has a prognosis of lasting more than a year; and

- Is diagnosed by a duly registered medical practitioner in accordance with the criteria prescribed by the Commissioner

In order to benefit from the full disability-related medical expenses provisions, you’ll need to have an ITR-DD (confirmation of diagnosis of disability form for an individual taxpayer) form completed by a registered medical practitioner.

Click on this link https://www.sars.gov.za/wp-content/uploads/SARS_ITR-DD_PD_E_v2023.13.00.pdf or email us at teresa@worldwidetax.co.uk for a copy of this form

What supporting documents do I need for SARS?

If you do claim medical credits as a result of paying medical aid for a dependent, where you are not the main member of the medical scheme, then it is almost certain that SARS will audit you. In this case, be sure you have the following:

- The medical aid tax certificate in the financial dependent’s name,

- Proof of payment to the medical aid (bank statements for that tax year)

- Letter explaining why this dependent is currently financially relying on you. (Please find below letter template)

Medical Aid contributions paid on behalf of a dependent

If you are claiming medical aid tax rebates on your personal return, but you are not the main member on the medical aid, we will need below related form completed and returned with your 2024 tax documents. You are only allowed to claim the medical aid tax rebates provided no one else is claiming this on their own returns.

Date

Taxpayer’s Full Name

Address

To Whom It May Concern,

Subject: medical aid contributions paid on behalf of a dependant

This letter serves to confirm that I, ________________________(taxpayer’s full name), __________________________(ID number) am contributing to a medical aid on behalf of _______________________________(name of dependant),___________________(ID number). He/she is/is not financially dependent on me and I am currently financially assisting due to: ________________________________________________________

I have been making medical aid contributions on behalf of my dependant for the following months:

_______________________________

Monthly contributions: R_________

Total annual contributions: R_________

Tax year: __________

Please see proof of payments attached.

______________________

Name

Relationship status e.g. Father

Telephone

Email

Medical Aid Monthly Rebates: