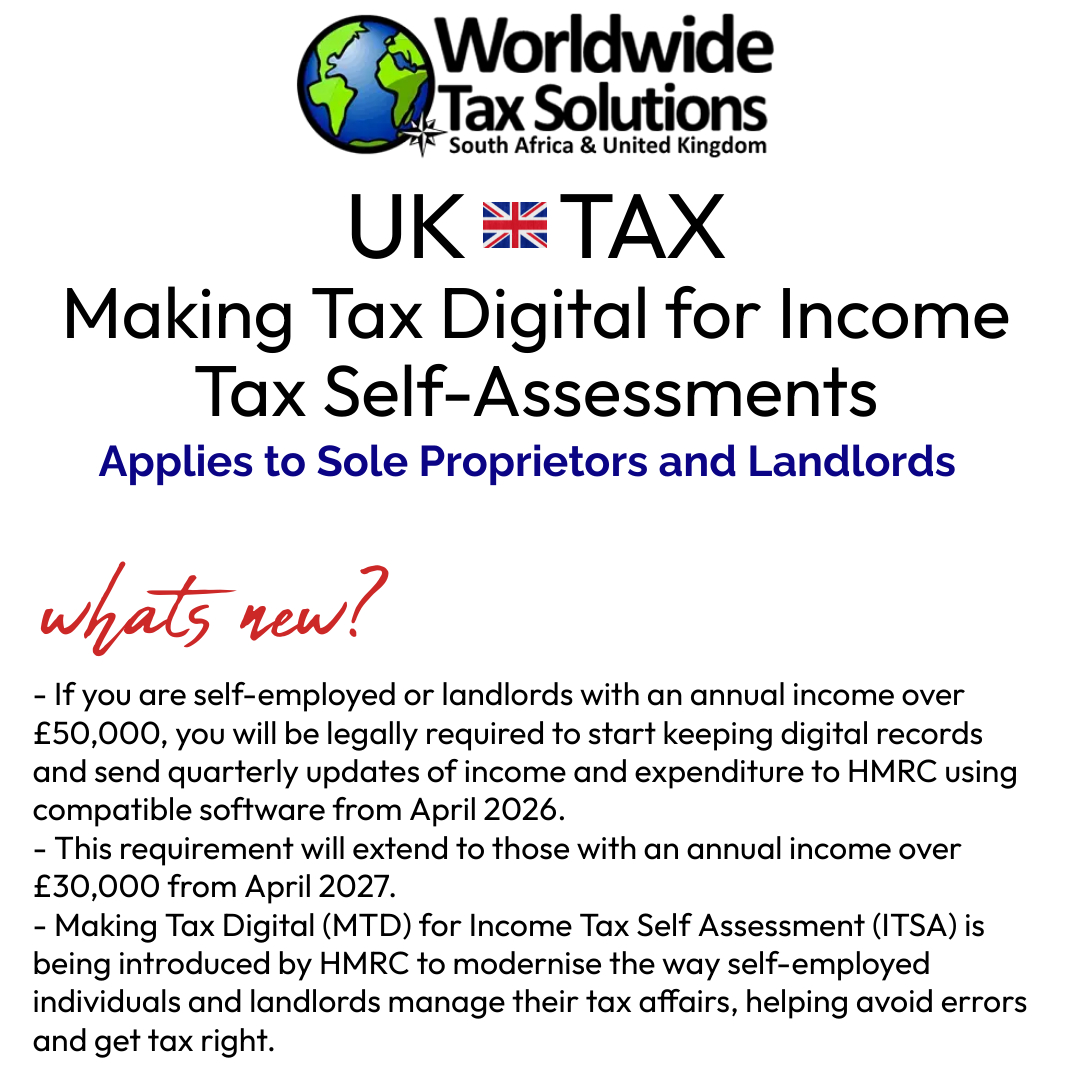

UK Tax Alert – Sole Proprietors and Landlords to send Quarterly Updates to HMRC

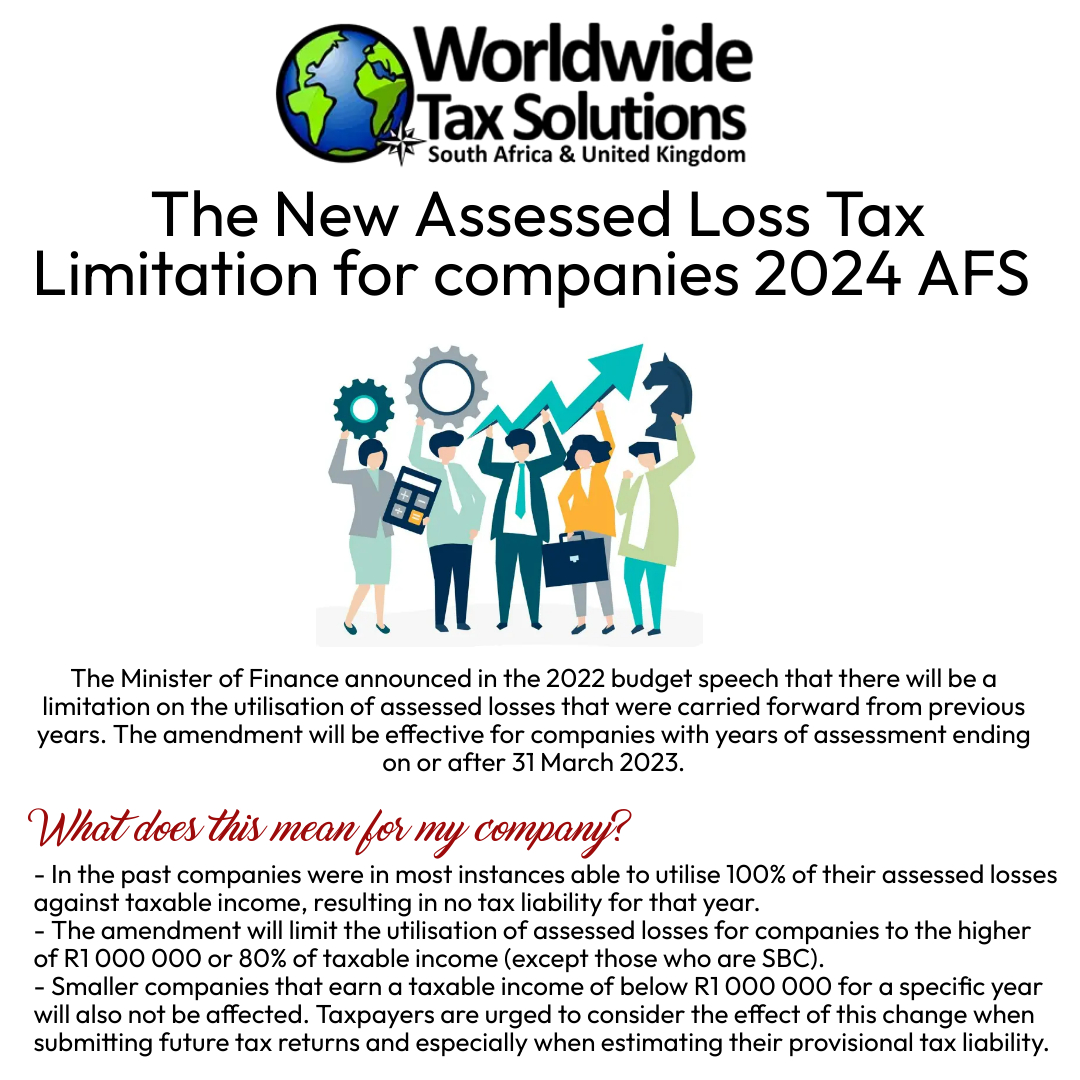

SARS Limited use of Assessed-Loss – Companies unable to use Full Assessed Loss against Future Profits

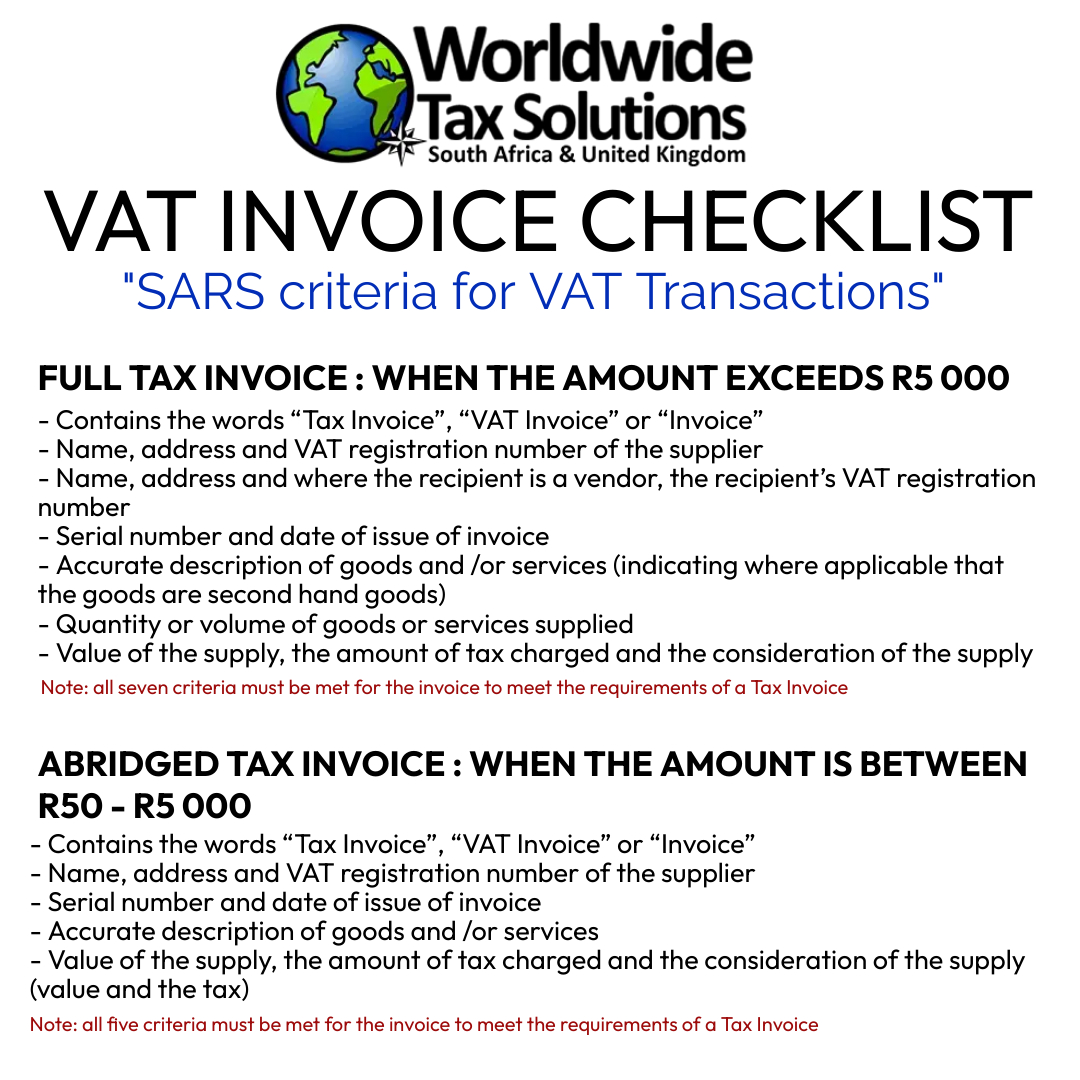

VAT Checklist – Criteria for Issuing and Receiving VAT invoices that are Acceptable to SARS

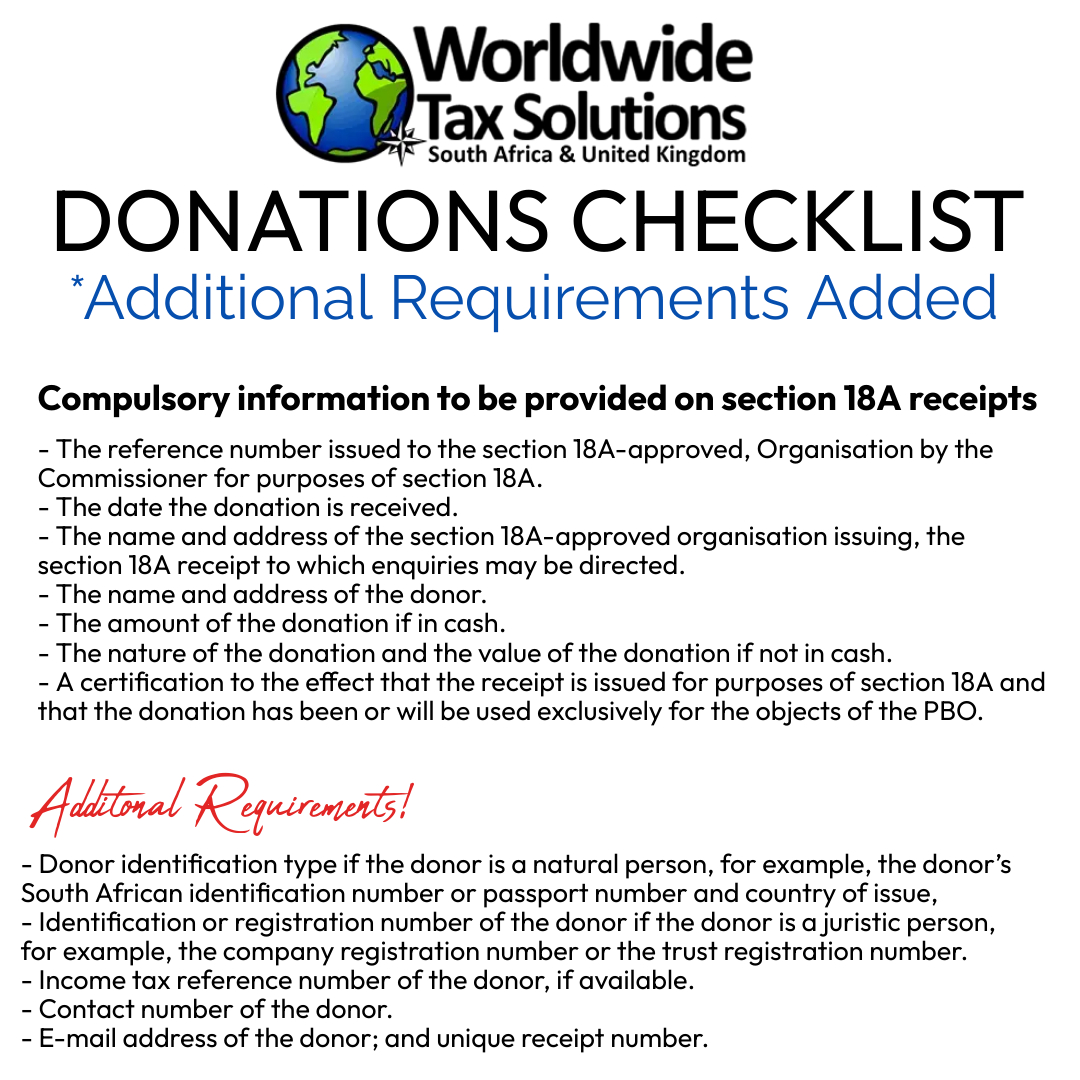

Donations Checklist – Applies to all Section 18a PBO Organisations

EXCITING NEWS!

Congratulations to our Director, Teresa Seaton, on being chosen as a SAIT Regional representative for the KwaZulu-Natal region. We are very proud of you! 🎉🏆

CCMA Rules change for Employees who earn more than R21 200

UNDERSTANDING SARS DISPUTES

The Office of the Tax Ombud dealing with SARS Disputes

The Office of the Tax Ombud (OTO) came to the rescue in a matter between the South African Revenue Service (Sars) and a taxpayer, ‘saving’ the taxpayer more than R500 000.

The taxpayer approached the OTO with its complaint when the objection it raised against an assessment was invalidated, preventing the taxpayer from lodging an appeal against the decision.

The dispute arose from a 2023 assessment in which Sars disallowed a claim for the tax exemption on income earned abroad.

The taxpayer objected and submitted supporting documentation for the claim.

Sars requested additional supporting documents, and the taxpayer obliged.

Sars did give reasons for rejecting the objection, and indicated that the taxpayer could submit a new notice of objection.

Following the invalidation of the objection, the taxpayer lodged a complaint with the OTO.

The OTO considered the matter and recommended that Sars withdraw the rejection and take a decision on the objection.

Sars adhered to the recommendation, allowed the dispute, and reduced the assessment by more than R500 000.

Sars can invalidate an objection if:

- The taxpayer does not set out the grounds of the objection in detail;

- The taxpayer does not use eFiling and does not specify the address where Sars can communicate with the taxpayer;

- The form is not signed or if the representative is not authorised to represent the taxpayer; or

- The objection is lodged more than 30 days after the date of the assessment.

There was no error in the objection; therefore, there was no defect to correct in a new notice of objection.

Sars’s reasons for the invalidation of the objection indicate that it had, in fact, considered the grounds of the objection and, thereby, the merits of the dispute.

It is thus evident that the reasons Sars gave for the invalidation of the objection fall outside the dispute resolution rules.

In the appeal process, alternative dispute resolution can be followed where the taxpayer and Sars meet to find a faster, less expensive solution.

The OTO notes that Sars is not allowed to invalidate an objection because it disagrees with the taxpayer’s grounds of dispute.

If Sars requests further supporting documentation – as it did in this case – it must decide to allow, disallow, or partially allow the objection based on the information submitted by the taxpayer.

Objections are “invalidly invalidated” more often than we would like to see. Although it is happening less frequently, it is still happening.

The 2020 Tax Ombud’s Systemic Investigations Report concluded that there was a 31% error rate where objections were incorrectly invalidated for various reasons.

There is no updated data to confirm whether the situation has improved or worsened.

If the objection is disallowed or partially allowed, the taxpayer can resubmit the objection to amend the non-compliance, or approach the OTO, as in this case, or the tax court to have it validated.

If Sars invalidates an objection, there is always something that can be corrected when submitting a new objection.

The taxpayer can submit the correct form, or properly set out the grounds for the objection, sign the form and supply an address if not using eFiling to address the non-compliance.

Generally, but not always, when Sars invalidates an objection, and you cannot address the reason for the invalidation in the next objection, it is an indication that the objection was invalidly invalidated.

National Treasury referred to the alternative dispute resolution proceedings during this year’s budget, noting that it can only be accessed at the appeal stage of a tax dispute.

Tax Obligations for Influencers

Income generated from influencer activities, including sponsored posts and partnerships on platforms is fully taxable and must be declared to the South African Revenue Service (SARS).

Dormant companies & the De-registration Process

What is a dormant company

A dormant company is classified as a company that has not actively traded for the full year of assessment.

Because there is no activity in the company, it’s easy to forget about it completely along with all red tape that goes with it.

Penalties

SARS have recently become a lot stricter about levying administrative penalties for non-submission and late submission of company tax returns (even if the company is dormant) and these penalties will continue to re-occur on a monthly basis until the submission of the tax returns.

So, if you’re director of a company or the public officer of a dormant company, you still have a duty to submit the company’s tax returns to SARS.

- Check with the Companies and Intellectual Property Commission (CIPC) to see which companies are registered on your name and identity number.

- You can also see here if the company is dormant or still active according to their records.

- Check on SARS eFiling to see if there are any outstanding tax returns for this company.

- Submit all outstanding tax returns to SARS and request the Tax Compliance Status.

De-register a company

When a company de-registers with the Companies and Intellectual Property Commission (CIPC), it implies the company is no longer registered and has no legal standing since it’s not doing any business nor has any assets or liabilities.

When a company de-registers with SARS, it will have no further tax obligations.

If you don’t intend to trade through your company, it would be advisable to de-register with both CIPC and SARS as soon as possible to avoid further administrative penalties.