New Scam Alert – Targeting Taxpayers this 2023 Tax Season:

A must-read for Landlords receiving Rental Income:

Receiving Rental Income? [A MUST READ]

What is rental income?

If an individual rents out a property (generally residential accommodation) and receives rental income, the amount received will be subject to income tax.

Residential accommodation can include:

- holiday homes

- bed-and-breakfast establishments

- guesthouses

- renting a section of your home, e.g. a room or a garden flat.

- dwelling houses and

- other similar residential dwellings.

How is tax calculated on rental income?

The rental income you receive should be added to any other income you may have but will also be reduced by certain permissible expenses incurred.

If any other amounts are paid to you for the rental of residential accommodation, in addition to the monthly rental, these amounts will also be subject to income tax.

The additional amounts can include, for example, lease premiums which are usually paid in the form of a lump sum at the start of the lease, in which case the full amount is subject to tax in the year of assessment during which it accrues or is received, whichever is the earlier.

The receipt or accrual of a rental deposit by a lessor need not be included in the lessor’s gross income at the stage it is initially paid, if there is an obligation on the lessor to refund the deposit at a later stage.

It will generally only become gross income in the lessor’s hands when the deposit is eventually applied by the lessor.

The treatment of a rental deposit should, however, be determined on the specific facts and circumstances of each case.

If you are married in community of property, please ensure both spouses are submitting their annual returns declaring their rental income and expenses.

If the property is owned jointly, please state your ownership percentage. Therefore, the profit/loss is apportioned accordingly.

Can the rental income be reduced?

Yes, the rental income may be reduced by any permissible expenses incurred during the period that the property was let.

Only expenses incurred in the production of that rental income can be claimed.

Any capital and/or private expenses will not be allowed as a deduction.

Which expenses are permissible?

Permissible expenses that may be deducted from rental income could include:

- rates and taxes

- levies

- water and electricity

- subscriptions

- accounting fees

- building insurance for property let out

- bond interest

- advertisements

- agency fees of estate agents

- insurance (only homeowner’s insurance and not insurance for household contents or bond insurance)

- garden services and cleaning

- repairs in respect of the area let and

- security and property levies

Which expenses are not allowed?

Expenses that are capital in nature or that are not in the production of rental income will not be allowed.

These can include, for example, costs for improvements made to the property.

Improvements should not be confused with repairs and maintenance which are allowed as a deduction.

Repairs and maintenance would usually take place when a person attempts to restore an asset to its original condition as a result of damage or deterioration.

Improvements would usually result in the creation of a better asset.

To determine whether a repair, maintenance or improvement has taken place, the specific facts and circumstances of each case must be examined.

While improvements are not allowed as a deduction against rental income, the value thereof can, however, be included in the base cost of the property, to effectively reduce the capital gain (or loss) on the eventual disposal of the property, for capital gains tax purposes.

The supply of accommodation in a dwelling is an exempt supply for VAT purposes, and consequently you may not deduct any VAT incurred on expenses in respect of supplying accommodation in a dwelling.

What if the expenses exceed the rental income?

Should the expenses exceed the rental income, the loss should be available for set-off against other income earned by the individual, provided that the loss is not “ring-fenced” in terms of prevailing anti-avoidance provisions.

The individual must effectively be able to satisfy SARS that he or she is carrying on a bona fide trade through the rental of his or her property.

If it is a shared property, please ensure that you state the square meterage of the entire property as a whole and the portion of the property been leased out.

Please note that you can only claim the portion of the expense of the leased property. Personal property expenses are not tax deductible.

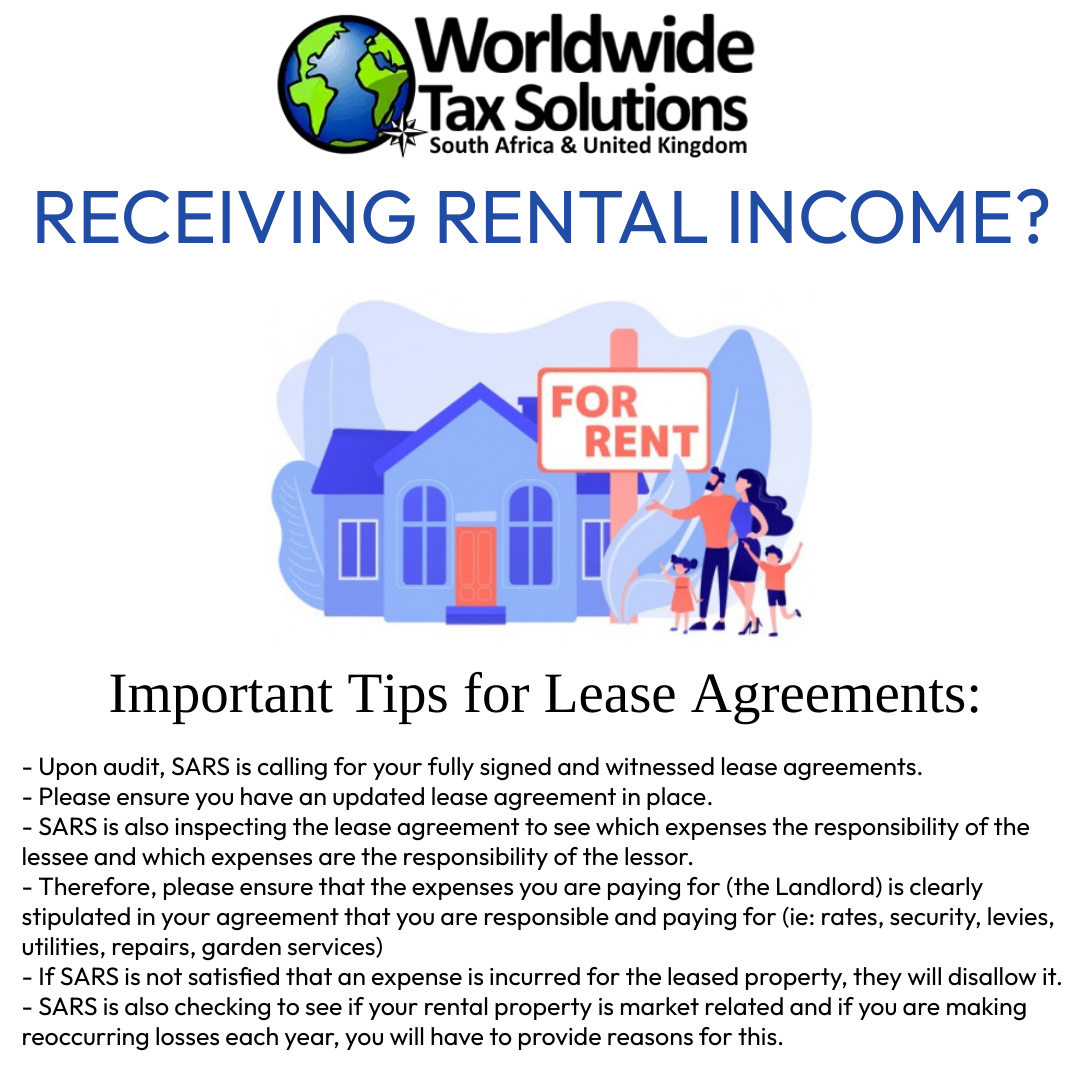

Important Notice: Lease Agreements

Upon audit, SARS is calling for your fully signed and witnessed lease agreements.

Please ensure you have an updated lease agreement in place.

SARS is also inspecting the lease agreement to see which expenses the responsibility of the lessee and which expenses are the responsibility of the lessor.

Therefore, please ensure that the expenses you are paying for (the Landlord) is clearly stipulated in your agreement that you are responsible and paying for (ie: rates, security, levies, utilities, repairs, garden services)

If SARS is not satisfied that an expense is incurred for the leased property, they will disallow it.

SARS is also checking to see if your rental property is market related and if you are making reoccurring losses each year, you will have to provide reasons for this.

Are you Married in ‘Community of Property’? How will this affect your Tax?

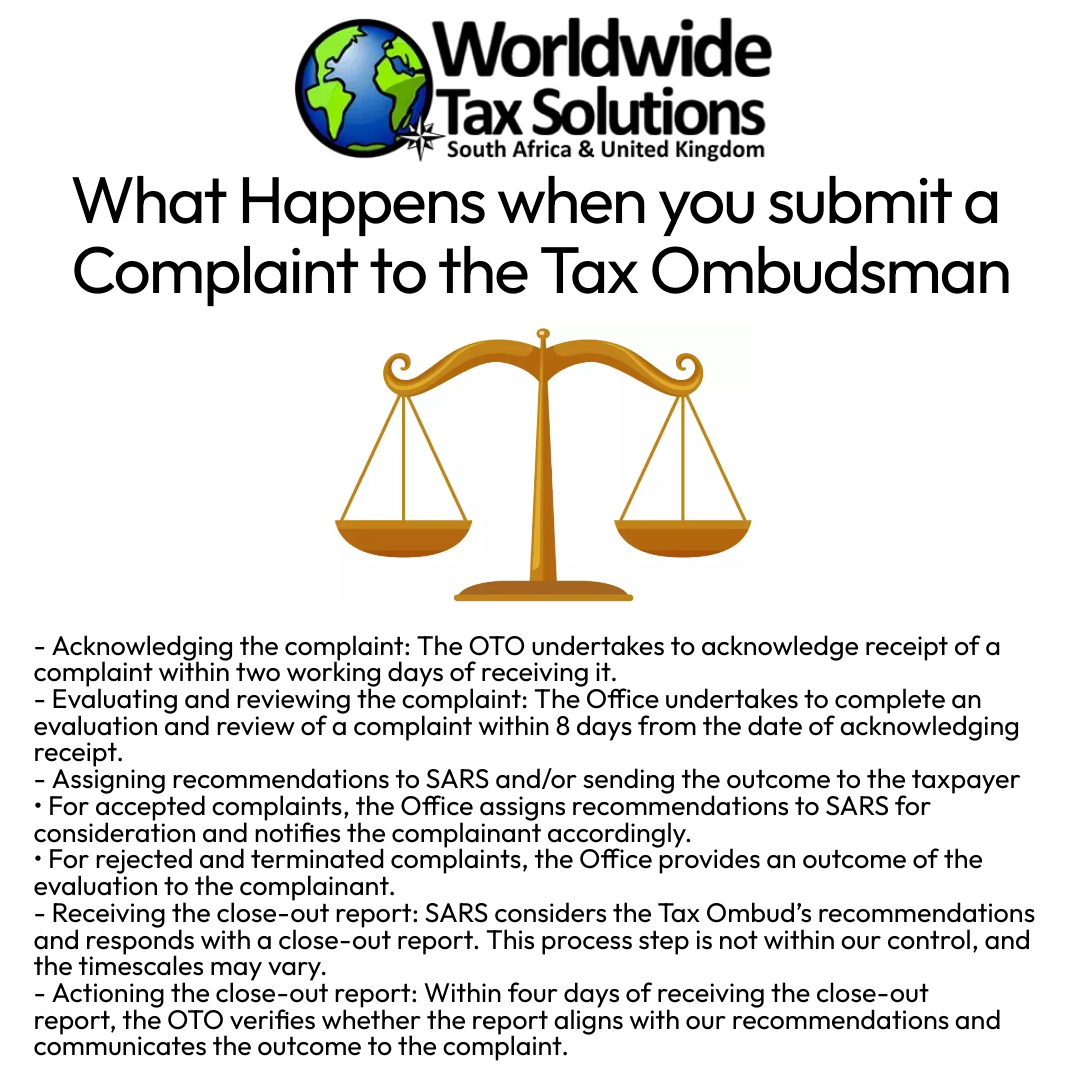

Everything you need to know about Submitting a Complaint to the Tax Ombudsman and the Supporting Documents to Prepare:

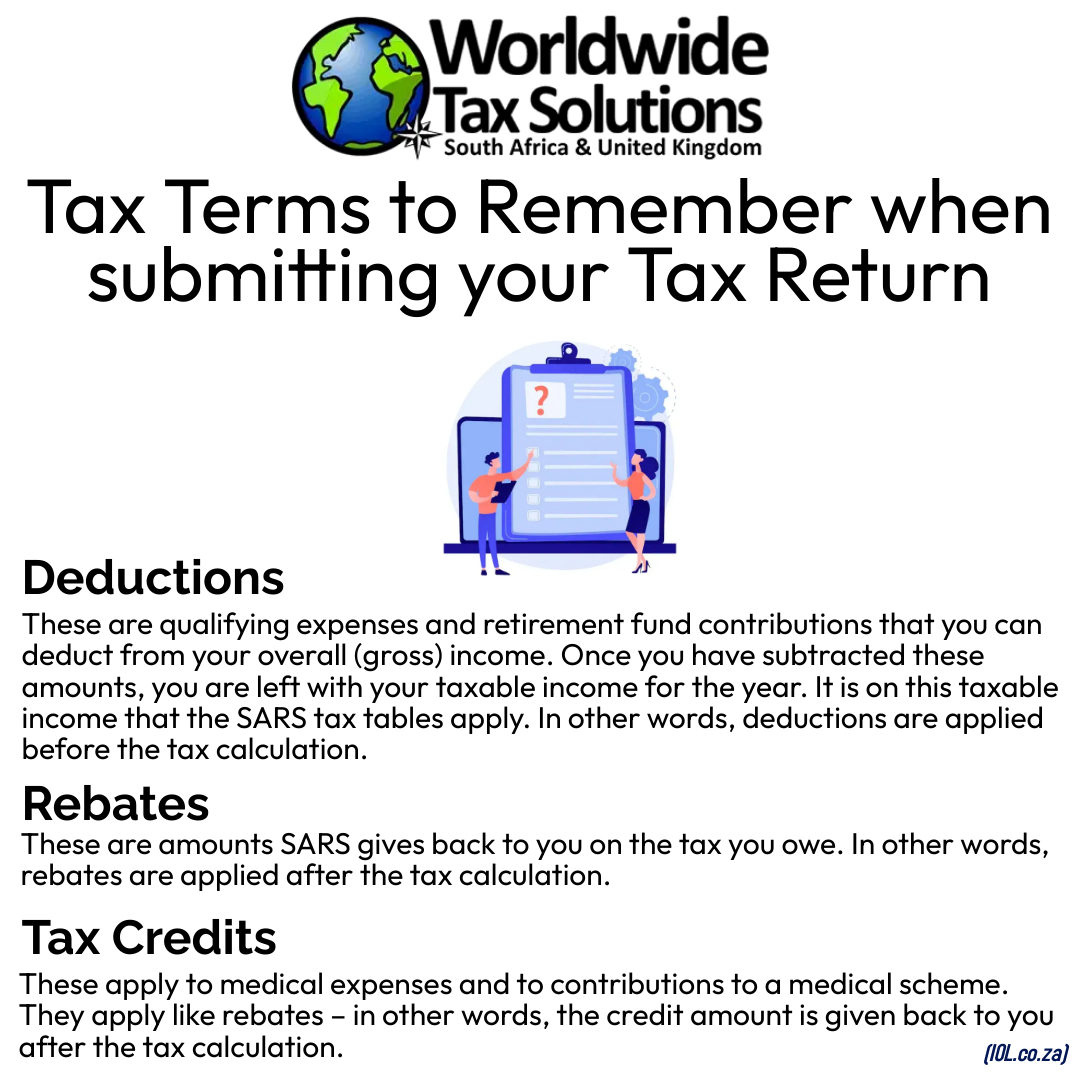

Tax Terms to Remember:

x Terms t

x Terms t

2023 Tax Season – Becoming a Client is Easy!

SARS is Fining Expats who have not Finalized their Tax Status:

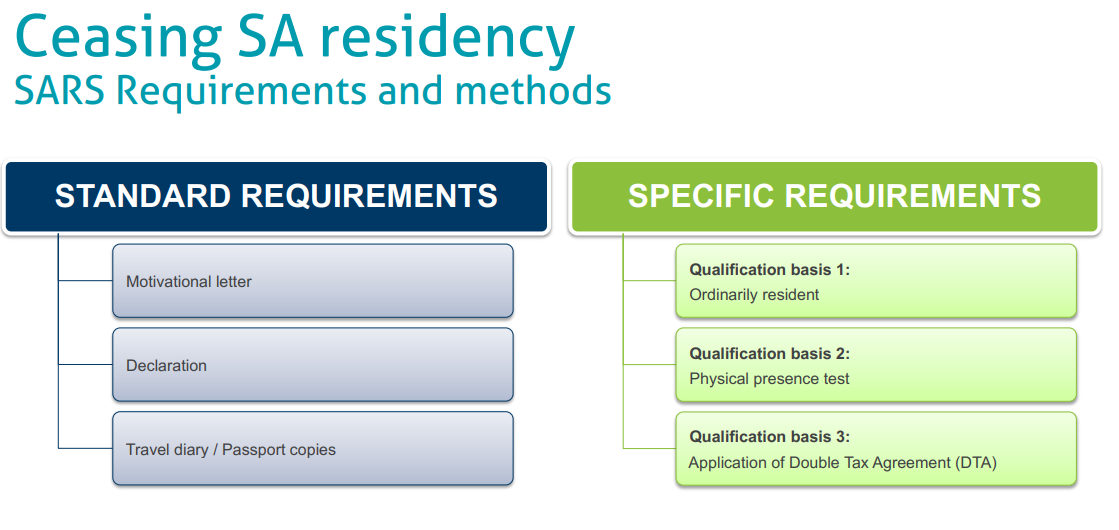

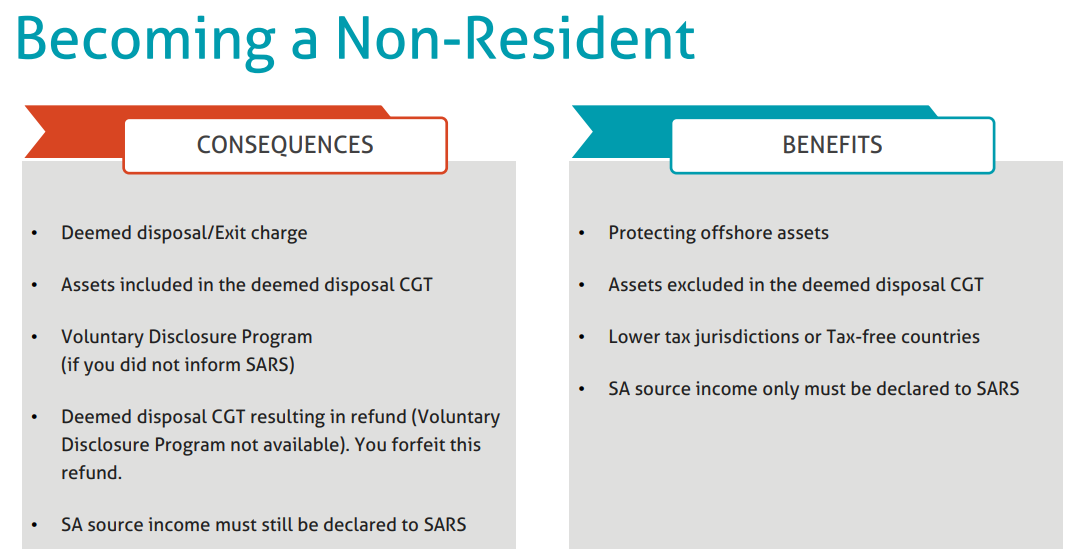

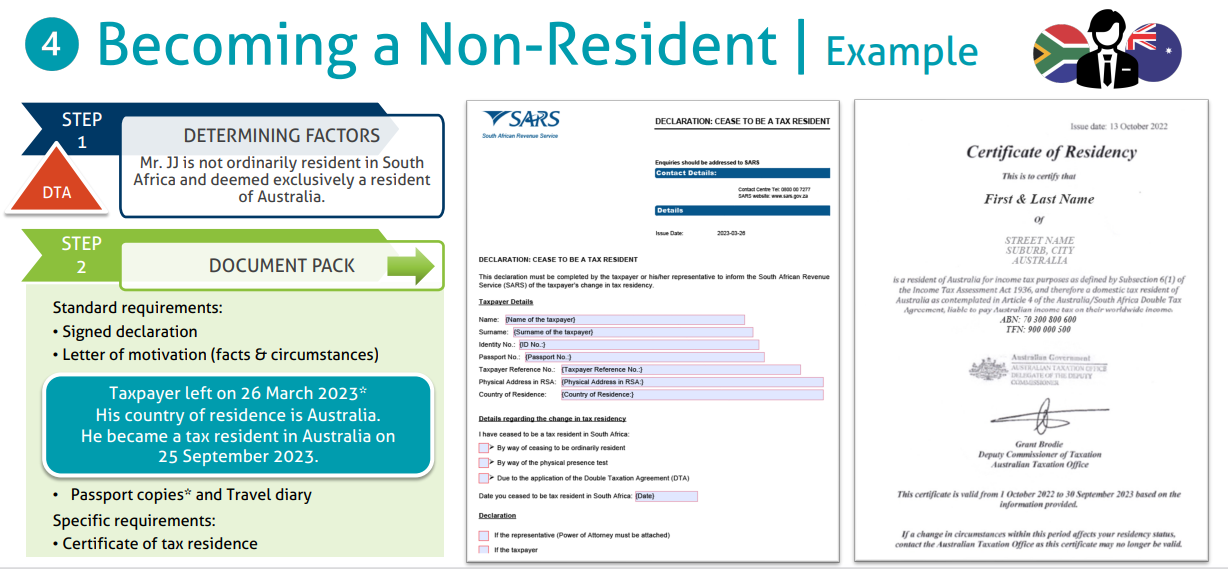

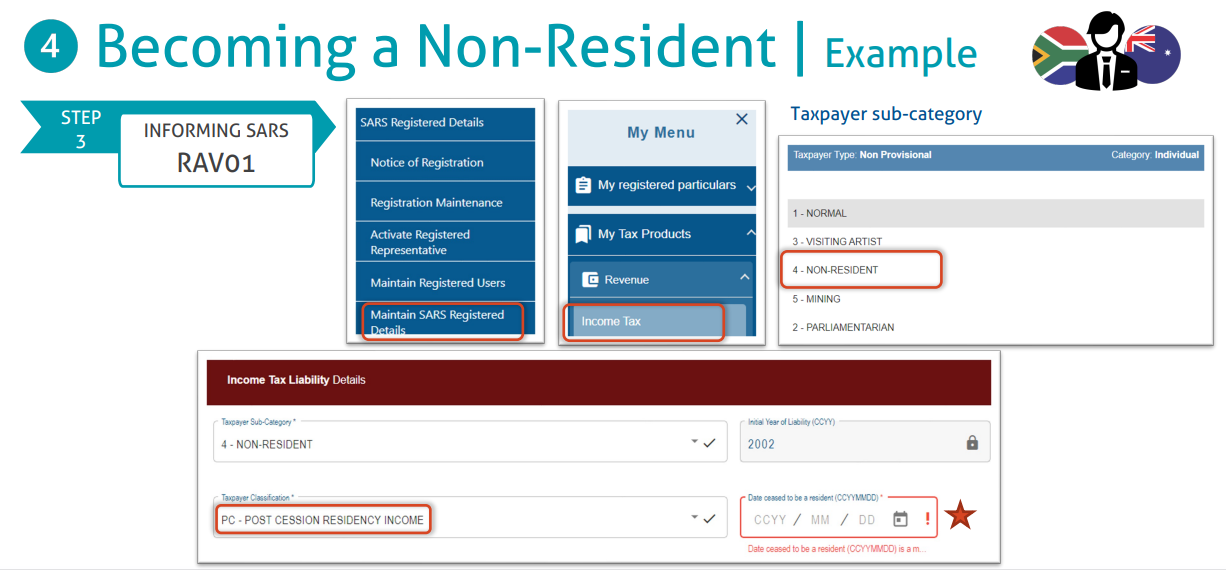

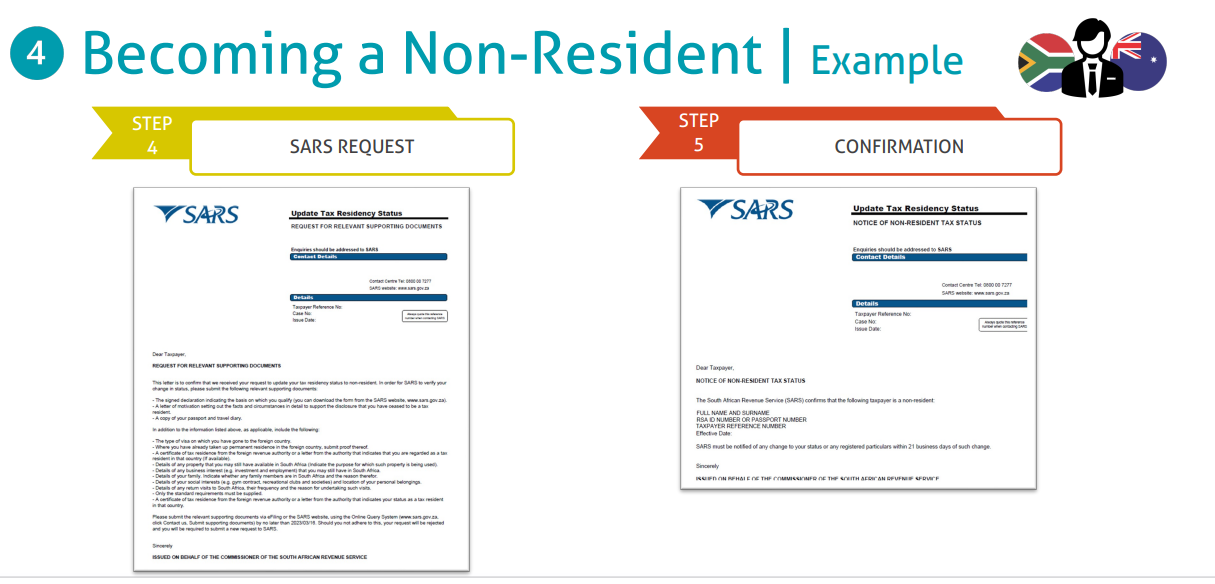

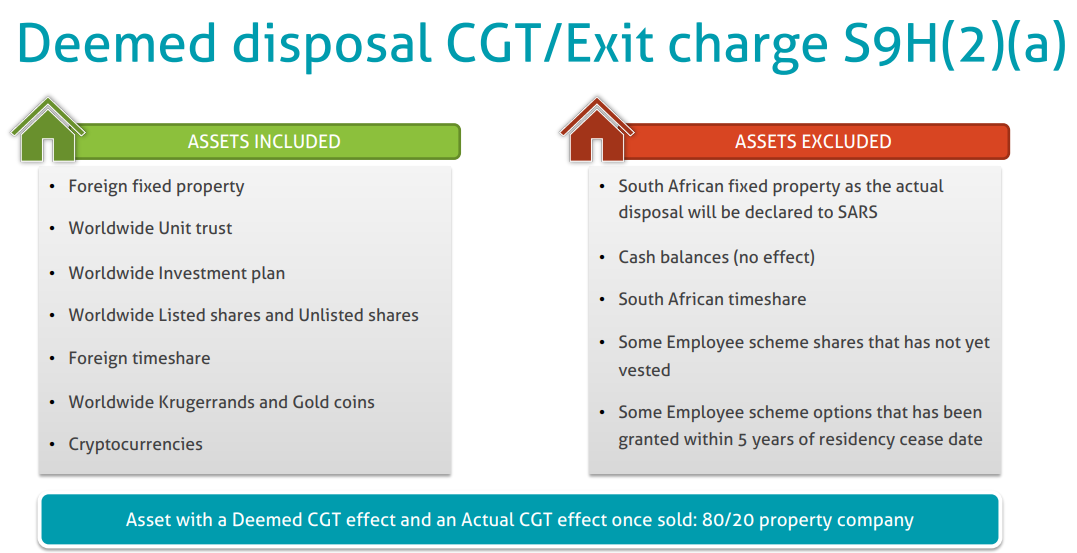

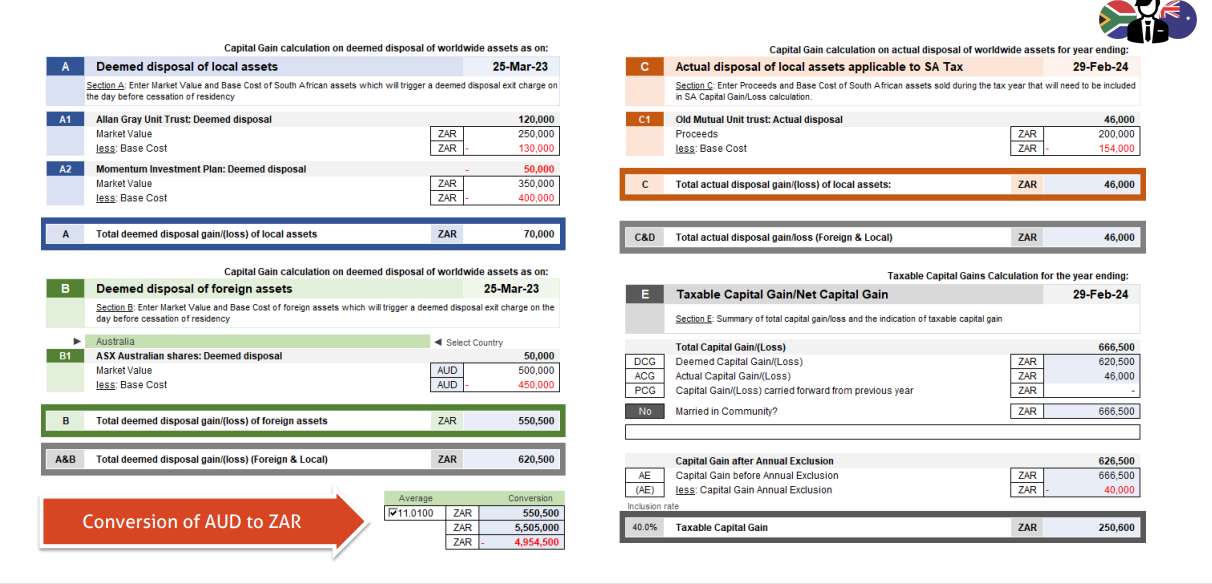

Everything you need to know about Ceasing your South African Residency.

This post includes:

- SARS Requirements and methods

- How to become a Non-Resident (Consequences and Benefits)

- Supporting Documents

- How to inform SARS

- Disposal CGT and Exit Charge explained, with examples.