Client Reviews still coming in after Tax Deadline:

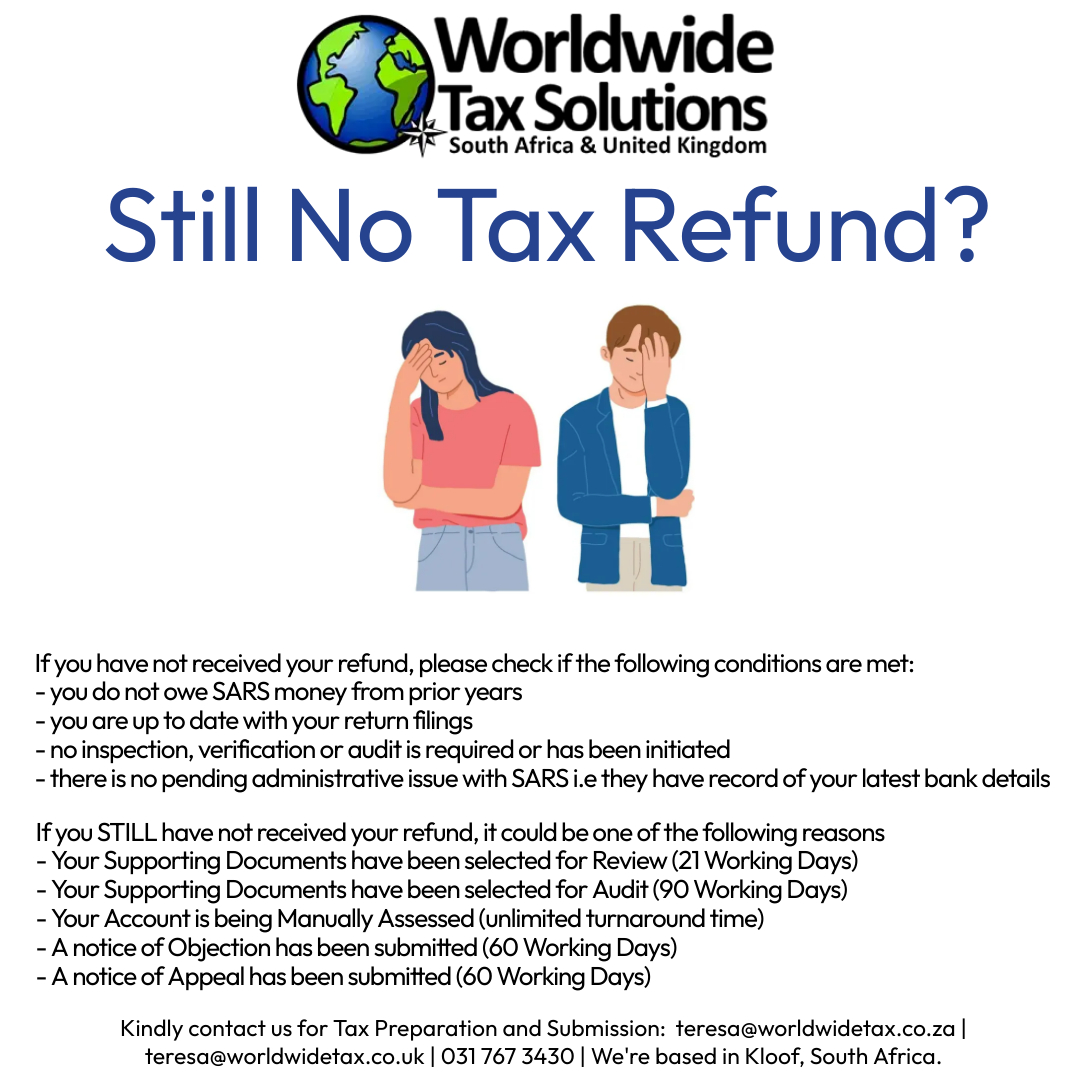

Still No Tax Refund? What is the Delay?

Sole Proprietor Tax Submission

TAX IMPLICATIONS FOR MARRIAGES IN COMMUNITY OF PROPERTY

The default marriage regime has some complicated tax consequences.

When couples are caught up in wedding and honeymoon planning, visiting their attorney often takes a backseat.

Many couples don’t realise that different marital laws affect how their assets are managed during marriage, divided if it ends, and how they’re taxed.

SARS made some updates to the 2023 personal income tax return. While most reporting requirements stay the same, the way SARS verifies the information is what’s drawing the most attention.

If you are married in community of property, a separate section for spouse details is opened, in which SARS requires your spouse’s initials and their ID number.

However, providing these details is more than a simple box-ticking exercise.

These include investment income (interest and dividends, both local and foreign), rental income, and capital gains and losses.

If you’re married in community of property, you’re taxed on half of your own and half of your spouse’s interest, dividends, rental income, and capital gains.

For any investment income that has not pulled through from a third-party upload, as well as for any rental income and capital gains or losses, you will need to provide the full amount of income received by both spouses in both of your tax returns.

SARS will automatically divide this income on a 50/50 basis.

This will be reflected on the notices of assessment (ITA34) issued to both you and your spouse once the returns have been submitted. Your returns do not need to be submitted simultaneously to achieve this split.

Some income types, by law, aren’t included in the community of property.

For instance, if someone inherits property or investments, and the deceased’s will specifically states it’s outside the communal estate, then it’s excluded.

Salaries have been taxed separately since the tax tables were harmonised in the early 1990s. This applies irrespective of one’s marital status.

If you and your spouse are separated and such separation is likely to be permanent, you would need to submit an RRA01 form to SARS or lodge an objection against your return.

If you and your spouse are divorced and you had omitted to amend your marital status from married in community of property to not married.

SARS will issue an amended assessment but is likely to request an upload of your divorce decree—particularly if the divorce was recent and the Home Affairs records have not yet been updated.

Client Reviews for 2023 Tax Season

We are incredibly grateful for the outpouring of gracious reviews from our clients. Thank you for your support.

202

202

Cyber-crime increase during Tax Season:

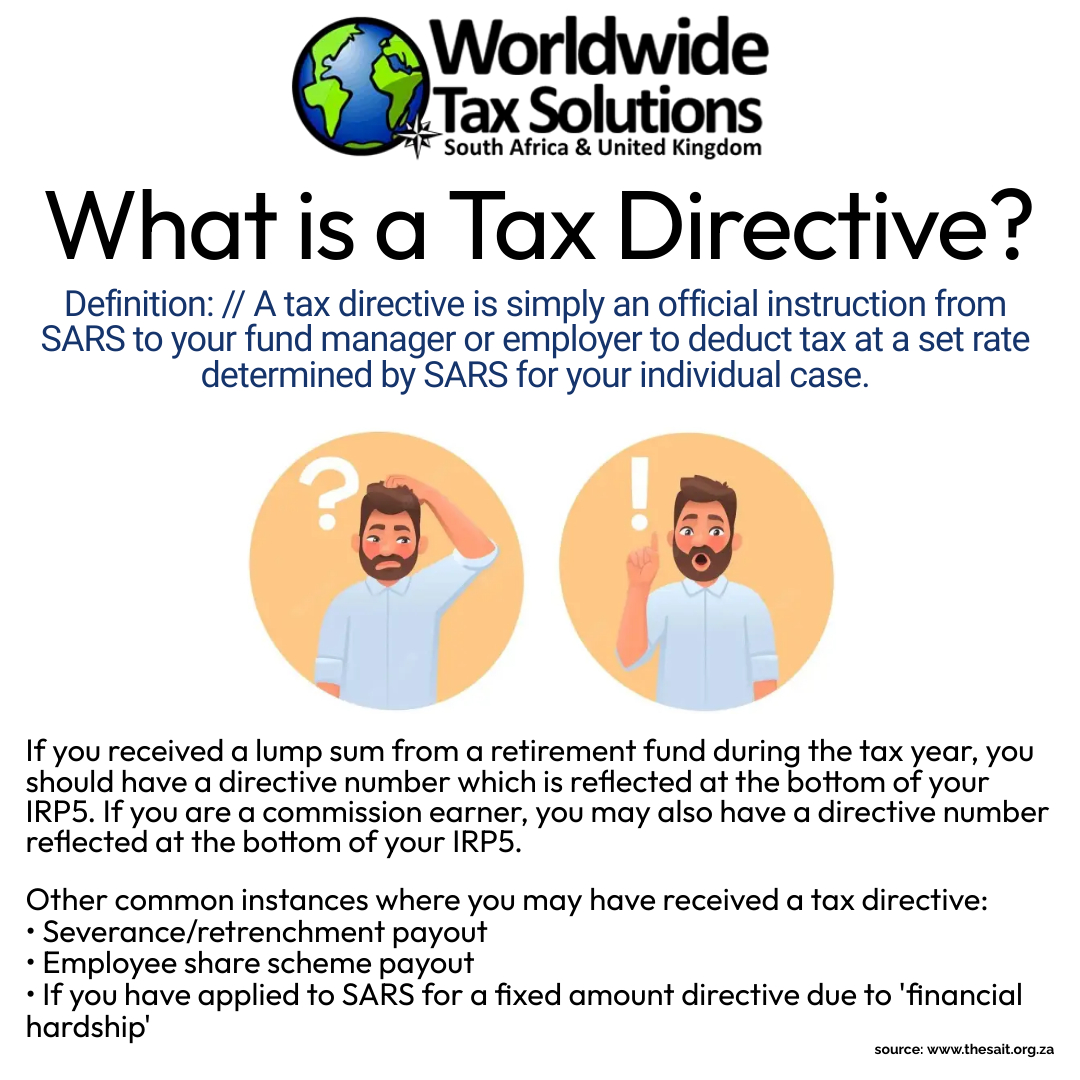

Tax Directive Explained:

Mid Term Budget Speech Date Announced